This woman was told her mortgage was paid off: 10 years later, she received a foreclosure notice in the mail. She decided to fight.

Aarthi Swaminathan – May 2, 2023

Mortgages originated in the early 2000’s and largely forgotten are now being pursued by debt collectors. Government officials are concerned.

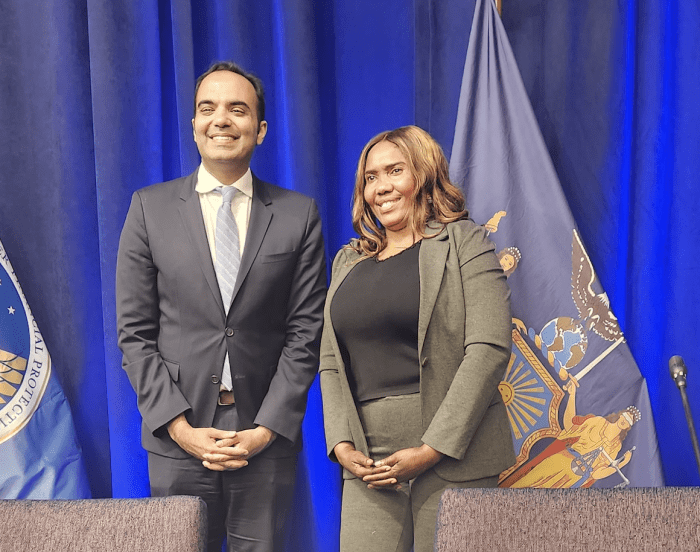

Rohit Chopra, director of the Consumer Financial Protection Bureau, stands beside homeowner Rose Prophete during a field hearing in Brooklyn, N.Y. PHOTO: LEGAL SERVICES NYC

Rose Prophete bought her home in Canarsie, Brooklyn, N.Y. in May 2005. She thought she had paid off her loans until recently, when a company approached her about a debt she thought she had settled a long time ago.

The company expected Prophete to pay up over $130,000, or face foreclosure.

When refinancing her mortgage on the home, Prophete had split her mortgage into two. Prophete said she had been erroneously told that her second mortgage was paid off. That debt, having laid dormant for years, was now being pursued by a debt-collection firm.

Prophete is one of 13 plaintiffs in a 2021 federal lawsuit against the firm, and she recently testified at a field hearing into “zombie debts” held by the Consumer Financial Protection Bureau, a government agency responsible for consumer protection in the financial-services sector.

The CFPB last week announced that it was issuing legal guidance for debt collectors trying to collect on mortgages that were long considered forgiven by borrowers, who in particular had no notices or statements sent over a decade about outstanding debt.

‘This is really frustrating — I don’t want to lose my home.’— Rose Prophete, who bought her home in Brooklyn, N.Y. in May 2005

The federal agency said that a debt collector “who brings or threatens to bring a state-court foreclosure action to collect a time-barred mortgage debt may violate the Fair Debt Collection Practices Act.” Time-barred refers to debt whose statute of limitations has run out.

“Debt collectors do not get to claim ignorance of the law or ignorance of the debt’s age,” Rohit Chopra, director of the CFPB, said during the hearing. “If the statute of limitations has expired, taking legal action threatening to bring a suit of foreclosure may be illegal no matter what the debt collector claims to have known. This is the law.”

Prophete, a Haitian immigrant and a hospital technician, said during the CFPB hearing that she had worked three jobs to afford the two-family Brooklyn home, on top of taking care of small children.

According to the lawsuit, a little more than a year after they completed the purchase, the broker who arranged the financing suggested she refinance the mortgage to lower her monthly payments. She agreed to refinance her mortgage into two, as the broker told her that this “financing structure would be the most financially advantageous to her,” per the filing. The first loan was for $504,000 and the second for $63,000 with an interest rate of 9%.

‘Debt collectors do not get to claim ignorance of the law or ignorance of the debt’s age.’— Rohit Chopra, director of the CFPB, speaking about the Fair Debt Collection Practices Act

After a couple of years, she received a note from her first lender that the second loan was fulfilled — that she didn’t need to pay for it. She said she didn’t receive any statements for the second mortgage, so she focused on paying off her first one, the lawsuit said.

She said she never heard back from the mortgage servicer, until over a decade later, in March 2021, when she received a foreclosure notice in the mail. The creditor was attempting to collect on payments due from Jan. 1, 2009 to the date of filing in 2021. The payments had ballooned from $63,000 to over $130,000, according to the lawsuit.

“This is really frustrating — I don’t want to lose my home,” Prophete said during the field hearing.

New York Attorney General Leticia James, who also spoke during the hearing, said that debt-collection firms were engaged in “predatory practices” to “rob individuals of the equity in their home.”

Debt buyers were acquiring these mortgages “often for pennies on the dollar,” James said, and they were now suing homeowners and “seeking to exploit rising housing values by reviving the long-dormant zombie debt.”

“I find this practice predatory and abusive and an affront to the American dream of sustainable home ownership,” she added. “I will fight this despicable practice.”

Florida’s insurance crisis: 2 special sessions, little help | Commentary

Scott Maxwell, Orlando Sentinel – May 2, 2023

For years, Florida lawmakers ignored a looming insurance crisis.

Then, with rates skyrocketing and companies fleeing the state, they scrambled to call not one, but two special sessions, vowing to help.

Well, my wife and I saw what the Legislature’s version of help looks like a few months ago when our insurance bill jumped from $4,000 to $7,000.

Any more “help “like that and we’ll be eating cat food.

In reality, we’ll be just fine. But a growing number of Floridians are facing bills they can barely afford as prices skyrocket throughout the state.

The Insurance Information Institute predicted increases of 40% throughout Florida this year. Some companies have requested 60% hikes. And scores of Floridians are still being dropped by their carriers while the state-run Citizens Property Insurance keeps bloating.

This is an undeniable, mounting mess.

So once again, GOP legislators – who have spent the better part of the past two years waging culture wars – have cobbled together another insurance bill.

But if you’re counting on this lowering your rates, bad news: It will not.

That’s not my take. It’s the take of former GOP Sen. Jeff Brandes – one of the few lawmakers who repeatedly warned his colleagues to take action years ago and was largely ignored.

“Nothing in this bill lowers rates,” Brandes, who now runs the Florida Policy Project, said this week. “Nothing in this bill encourages more companies to come.”

Brandes and I have differing views on some aspects of reform – particularly as it relates to the transparency measures and regulations that subsidized insurance companies should face.

But we agree on three key things:

1. Despite years of yapping about fraud claims driving up costs and rates, Florida lawmakers have never cracked down on bad actors in any meaningful fashion.

2. The solutions they’re talking about now aren’t going to do much, if anything, to bring down rates.

3. Any meaningful solution – in a state like ours that’s basically a bullseye for hurricanes and increasingly at risk of flooding – is going to involve a boatload of public money.

Brandes and I may have varied thoughts on how that money should be spent. But the reality is that this problem – where the state-run insurance company is now covering millions of Floridians at increasingly high rates – requires a major investment and serious policy reform.

And that’s not good news for a Legislature that specializes in divisive bumper-sticker priorities – dragging Disney, fuming about drag queens and decrying wokeism.

When it comes to hard, serious policy work, they are either unwilling or incapable of getting the job done. At least when it comes to insurance.

A clear example of that is fraud. For years, lawmakers have blamed fraudulent claims for driving up insurance costs and driving companies out of the state. But they haven’t done squat from an enforcement standpoint.

“If you want talent in the Office of Insurance Regulation – which should be one of the most talented in the state – you have to pay for it,” Brandes said.

That seems obvious. If your city had a rash of burglaries, you’d beef up your burglary patrol. But Florida politicians have whined about fraud without ever dedicating serious resources to exposing, punishing and stopping it.

If they can set up a statewide election-crime police force to deal with fever-dream problems, you’d think they’d beef up their insurance team to deal with an actual financial nightmare.

But to really bring down prices, we need more competition among providers. Or we need to invest more in Citizens – and basically accept that a giant, costly state-run insurance company is the only way we’re going to be able to cover everyone in a state that’s both storm-ravaged and low-wage.

Few people really want that second option. Certainly not Brandes. But many of us aren’t super keen either on just handing over tax dollars to an industry with a track record of hosing its policy holders.

Just a few weeks ago, the Washington Post published a maddening investigative report that found Florida insurance companies were financially victimizing hurricane survivors by gutting their claims and payments – sometimes by as much as 90% of what the companies’ own adjusters said the homeowners were due. The piece featured an adjuster who said one insurance company took his report – which estimated $200,000 in valid claims for one home – and whittled it down to just $27,000 without his knowledge or consent.

Brandes prefers offering companies incentives to write Florida policies. That may be worth exploring – with a lot of checks and balances added in.

But here’s the bottom line: Either scenario – majorly subsidizing private industries or growing/transforming Citizens into something like a Florida version of Medicare for homeowners – is painful. They’re both costly, politically unpopular and involve a lot of hard work.

Unfortunately, most Florida politicians don’t want to do hard work or make unpopular moves. So they just keep screaming about critical race theory and transgender athletes. And while they scream, your rates keep rising.

I think we’re heading toward a pain point – where even the Floridians who used to laugh at the culture wars are going to stop laughing once they realize they can barely afford to stay in their homes. That may be when they start finally putting people in office who are more interested in solving problems than creating them.

The uptick on excoriating “woke ” ideology has increased in recent years among politicians, including former President Donald Trump, as Americans across the nation battle over diversity, inclusion and equity efforts in the workforce, public schools and in legislation.

But what is “woke”? And what do the GOP attacks mean for 2024?

Among conservative lawmakers and activists “woke” tends to be an across-the-board denunciation of progressive values and liberal initiatives.

Some have used it to attack trans and gay rights while others apply it to critical race theory – a legal theory that examines systemic racism as a part of American institutions – and the teachings of the New York Times’ 1619 project in public schools.

“If you ask people what woke is, I think what they mean is they want to stand against people who are engaging in some type of advocacy for marginalized people,” said Andra Gillespie, political scientist at Emory University.

“It’s kind of this lumping together of anybody whose views could be construed as being progressive on issues related to identity and civil rights.”

As the Black Lives Matter movement began after the police killing of Michael Brown in Ferguson, Missouri in 2014, “woke” expanded outside of Black communities into the larger public lexicon.

What about ‘stay woke’?

Black artists and entertainers continued to insert the phrase in their music, including Grammy-award-winning artists Erykah Badu and Childish Gambino — a.k.a. Donald Glover—for political causes.

Yet “woke” has now been hijacked by the political right to mean something far from its original definition.

“The reason we have to ‘stay woke’ is because of exactly what these people are doing right now, which is finding very insidious ways to undercut our rights,” said Terri Givens, a political science professor at McGill University.

Givens called the attacks on the term “a full-on dog whistle” and pointed to attempts to limit the right to vote, curtail reproductive and abortion rights and ban inclusive education in schools as examples of the backlash against Black and brown civil rights.

“Learning history is not about woke-ism,” Given said.

Conservatives now use the term as a political retort to combat what they perceive as political correctness gone haywire.

But progressive commentators note that the response also comes in the context of a changing America, which is becoming more diverse racially and ethically and along sexual orientation and gender identity lines.

“What they’re trying to do is make the term a pejorative,” said Kendra Cotton, chief operating officer of New Georgia Project, a progressive-leaning voting rights group.

As more marginalized groups are elected into office and exercising their voting power during elections, it can make some Americans afraid, said Cotton.

Florida Gov. Ron DeSantis, a possible GOP presidential candidate, has built a persona crusading against ideas and policies conservatives deem as “woke.”

Tehama Lopez Bunyasi, a political scientist at George Mason University and co-author of the book “Stay Woke: A People’s Guide to Making All Black Lives Matter,” said the legislation is “perhaps the most explicit way we see the co-optation of the term ‘woke’ today.”

“Right now, we’re seeing racially conservative pundits and politicians positioning themselves as adversaries of the multiracial Black Lives Matter movement,” said Lopez Bunyasi. “One of the rhetorical tools they are using is the maligning of a term that has been in use by Black people and in Black politics for well over a hundred years.”

Have the anti-woke attacks been successful?

Virginia GOP Gov. Glenn Youngkin cruised to victory in 2021 riding a wave of parental anger over teaching inclusive history in public schools.

Keneshia Grant, a political scientist at Howard University, said Youngkin’s success was part of an intentional pushback against marginalized communities, which includes misunderstanding terms like woke, critical race theory, and LGBTQ rights.

“He ends up successfully using the fear that people have about teaching students Black history or American history through the guise of CRT and successfully uses that to motivate a base,” Grant said. “They are doing this because they think it will help them win. And we have evidence that sometimes it actually does help them win.”

Americans divided on what ‘woke’ means

What’s telling is that despite the conservative backlash most Americans don’t view “woke” negatively heading into the 2024 presidential contest.

A March 2023 USA TODAY/Ipsos Poll found that 56% of Americans said it means “to be informed, educated on, and aware of social injustices.”

But the efforts to re-define “woke” have worked with a significant portion of the country. Roughly 39% of those surveyed agree with the Republican definition,”to be overly politically correct and police others’ words.”

“Racial resentment and grievance are certainly one of those things that have been very effectively used to mobilize a certain segment of the Republican population for a long time,” said Gillespie.

Reporter Phillip M. Bailey contributed to this story.

Disney v. DeSantis judge called Florida governor’s law ‘dystopian’

Tom Hals – April 26, 2023

WILMINGTON, Delaware (Reuters) -When attorneys for Florida Governor Ron DeSantis appear in court to defend against Walt Disney Co’s lawsuit that accuses the Republican official of weaponizing state government, they will see a familiar face, if not always a welcome one.

U.S. District Judge Mark Walker in Tallahassee has struck down several laws that defined DeSantis’ conservative political agenda, including statutes that sought to limit the speech of college professors, curtailed protests and restricted voting access.

Walker was nominated to the federal court by former President Barack Obama, a Democrat.

Disney sued DeSantis on Wednesday to block a state law that created an oversight board that Disney said will interfere with billions of dollars of planned development.

The feud between the global entertainment giant and a likely candidate for the 2024 presidential election started last year, when Disney criticized a law signed by DeSantis that banned classroom instruction on gender identity and sexual orientation for younger children.

Disney alleges a law that imposed an oversight board was punishment for voicing opposition to DeSantis’ classroom instruction law known as the Parental Rights in Education Act.

The company called the state’s actions “particularly offensive here due to the clear retaliatory and punitive intent.”

The gender-education statute, derided by critics as the “Don’t Say Gay” law, survived challenges in federal court before a different judge.

Free speech has been central to several rulings by Walker against DeSantis, although the judge has also at times sided with the governor.

Walker blocked the Individual Freedom Act or Stop Woke Act, which limited the speech of college professors, calling it “positively dystopian” in an opinion that began with a quote from George Orwell’s anti-totalitarian novel “1984.”

In 2021, Walker blocked the Combating Public Disorder Act, which DeSantis signed into law after the 2020 protests over the murder of George Floyd, a Black man, at the hands of police.

Walker ruled the law’s expansion of the definition of “riot” infringed on protesters’ right to free speech.

The judge last year enjoined a law signed by DeSantis that banned ballot drop boxes and prevented groups from offering food and water to voters waiting in long lines, causes championed by Democrats as a way to support voter turnout.

The judge also sided with plaintiffs in a second lawsuit challenging a different aspect of the Stop Woke Act, which defined as “unlawful employment practices” workplace training around issues of race and sex.

Walker said Florida had become a place where the First Amendment allowed, rather than prevented, the state to limit speech. Or as he put it, “in the popular television series Stranger Things, the ‘upside down’ describes a parallel dimension containing a distorted version of our world. Recently, Florida has seemed like a First Amendment upside down.”

The judge has also ruled with DeSantis and declined to block the execution of a death row inmate and dismissed some claims against the governor over the Individual Freedom Act.

(Reporting by Tom Hals in Wilmington, DelawareAdditional reporting by Lisa Richwine in Los AngelesEditing by Amy Stevens and Matthew Lewis)

First Republic handed out billions in ultra-low-rate mortgages to the wealthy. It backfired horribly.

Matt Turner – April 25, 2023

Lucas Jackson/Reuters

First Republic is teetering, with the stock down 93% in 2023 and the bank exploring strategic options.

The bank won wealthy clients with the offer of jumbo mortgage loans that required no principal payments for a decade.

The bank is now reversing course as it fights for survival.

First Republic is racing to strengthen itself.

The bank said Monday that it will cut as much as 25% of staff, and is pursuing strategic options after revealing that deposits plunged by more than $100 billion in the first three months of the year.

That sent the stock as much as 48% lower on the day, with First Republic now down 93% for the year to date. Gillian Tan and Matthew Monks at Bloomberg subsequently reported that the bank is exploring an asset sale in the range of $50 billion to $100 billion.

First Republic first moved into focus back in the March banking crisis that claimed Silicon Valley Bank, Signature Bank, and Silvergate.

Like SVB and Signature, a large percentage of First Republic deposits were not insured by the FDIC, making it especially susceptible to deposit flight. Like SVB, First Republic had seen deposits boom in the low-rate pandemic era. And like SVB, First Republic has been sitting on large unrealized losses, as the value of the bonds it’s marked as being held-to-maturity has dropped as rates have gone up.

One of the causes of First Republic’s troubles is a strategy to woo rich clients with huge mortgages that offer sweet terms, as detailed in this story from Noah Buhayar, Jennifer Surane, Max Reyes, and Ann Choi at Bloomberg.

In particular, First Republic would offer interest-only mortgages, where the borrower didn’t have to pay back any principal for the first decade of the loan. In 2020 and 2021, it extended close to $20 billion of these loans in San Francisco, Los Angeles, and New York alone, per Bloomberg’s analysis.

Many of these loans went to ultra wealthy types in finance, tech, and media. For example, one of the most senior executives at Goldman Sachs took out an $11.2 million mortgage with First Republic with no principal payments in the first 10 years and an interest rate below 3%, per Bloomberg.

The quality of these loans isn’t in question, as the borrowers are extremely safe bets.

But the loans are worth a lot less now than when First Republic wrote these deals, with the average mortgage rate on a thirty-year fixed rate loan now at around 6.3%. (Bond prices go down as interest rates go up, and vice versa.)

Wealthy clients can easily move their deposits away from First Republic while keeping their mortgage with the firm, which creates a liquidity challenge.

And these loans are hard to sell to other lenders, given Fannie Mae and Freddie Mac are limited to only purchasing mortgages up to just over $1 million. Should they successfully sell, it would also create a hole in First Republic’s balance sheet. The bank would be forced to recognize the current value of these loans, and what are currently unrealized losses could suddenly wipe out the bank’s capital.

First Republic is now backtracking from this strategy, saying it will focus on writing loans that are guaranteed by Fannie and Freddie.

More immediately, the bank is trying to find a way to convince buyers to take on some of its assets, including finding ways to sweeten the deal with equity-like instruments so buyers pay a higher price for the loans, according to Tan and Monks at Bloomberg.

The coming days will show whether First Republic was successful.

Can lawmakers save the collapsing Florida home insurance market?

Cate Deventer – April 24, 2023

Hurricane Ian could be ‘one of the most severe loss events in U.S. history’: Insurance expert

Insurance Information Institute Director Mark Friedlander joins Yahoo Finance Live to discuss the fraud and over-litigation in Florida’s insurance markets, the losses expected from Hurricane Ian, and insurance reform legislation.

The Florida home insurance market has spent most of 2022 tumbling toward collapse, but recent legislation just might avert disaster. Bankrate dug deep into the Florida insurance industry to discover the cause of the problem and to report on the proposed solutions. We can help you understand why the Florida home insurance crisis is happening and your options if you receive a cancellation or nonrenewal notice on your homeowners insurance policy.

Lightbulb Key insights Governor Ron DeSantis signed a second insurance reform bill into law on December 16, 2022. Combined with earlier legislation, these new regulations may stabilize the spasming home insurance market.

Florida accounts for only 9 percent of the country’s home insurance claims but 79 percent of its home insurance lawsuits, many of them fraudulent. Because of the fraudulent lawsuits and the high overall claim risk in Florida, insurance companies have faced two consecutive years with net underwriting losses over $1 billion. The devastating damage from Hurricane Ian will likely put further strain on Florida insurers and could worsen the crisis.

The crisis in the Florida insurance market

Florida has always been a complex home insurance market, but recent issues are pushing the state’s market to the point of collapse. Since 2017, six property and casualty companies that offered homeowners insurance in Florida liquidated. Five more are in the liquidation process in 2022. Other insurance companies are voluntarily leaving the state. Even more are choosing to nonrenew swaths of home insurance policies, drastically tighten their policy eligibility requirements or request substantial rate increases.

For Florida homeowners, this is resulting in fewer home insurance companies and increased premiums. When a company goes insolvent, the Florida Insurance Guaranty Association (FIGA) takes on any claims that still need to be paid by that company. In late August, FIGA’s board and the Florida Office of Insurance Regulation (OIR) approved a .7 percent assessment to help cover the costs of open claims associated with the liquidated companies. That’s the second assessment this year, with a 1.3 percent assessment approved in March. Homeowners will pay these fees regardless of the insurance company they are with.

According to Logan McFaddin, Vice President of State Government Relations at the American Property Casualty Insurance Association,

Florida’s property insurance market is in crisis as insurers grapple with out-of-control litigation costs and billions in losses from recent natural disasters.

Florida’s Insurance Consumer Advocate (ICA) Tasha Carter agrees, saying, “Homeowners insurance options in Florida have become more and more limited, and consumers are facing dire consequences.”

Why are home insurance companies leaving Florida?

Florida insurers are canceling policies, leaving the state or liquidating at a rapid pace. Why? What is behind these companies’ aversion to insuring Florida homes?

Florida has always presented a risky market to home insurance companies due to the high threat of widespread weather-related damage, but the current crisis is caused by a number of factors reaching a boiling point at the same time.

Insurance fraud in Florida

The biggest issue right now in Florida is home insurance fraud, driven by fraudulent roofing claims. A proclamation from the office of Governor Ron DeSantis notes that, although Florida only accounts for 9 percent of the country’s home insurance claims, it is home to 79 percent of the country’s home insurance lawsuits. Many of these lawsuits are fraudulent. ICA Carter explains how the scams generally work:

First, roofers canvas neighborhoods and offer inspections to unsuspecting homeowners. These contractors inevitably “find damage” on the roof and often promise a “free roof” to the homeowner, claiming they can have the home insurance deductible waived.

Homeowners are pressured to sign an assignment of benefits form, giving contractors the right to file an insurance claim on their behalf.

A claims adjuster from the insurance company inspects the alleged damage. The adjuster either finds no damage or far more minimal damage than the contractor found, and the claim payout is less than what the contractor demanded.

The contractor brings legal action against the insurance company, demanding a claim payout for the contractor’s original quote. Remember, the homeowner signed the benefits of the policy to the contractor, so the contractor doesn’t need the homeowner’s permission to do this.

The insurance company now has a choice: it can pay the legal costs to fight the lawsuit or pay the costs to settle out of court. Either way, the insurance company loses money due to the legal action.

ICA Carter notes that “these schemes are real and are happening more frequently,” which puts more and more financial pressure on insurance companies, especially in a state with high claims costs due to weather-related events.

According to Mark Friedlander, Director of Corporate Communications at the Insurance Information Institute, “Florida property insurers are projected to post a cumulative underwriting loss of $1.7 billion for 2021” due to these runaway litigation costs. The governor’s office reports that, for two consecutive years, net underwriting losses have exceeded $1 billion. It’s no wonder that so many companies are going insolvent or leaving the state before they reach that point.

On top of that, Florida also previously had a “one-way attorney fee” system. This meant that, when a court ruled in favor of the plaintiff (in this case, a home insurance policyholder or the third-party contractor who filed the claim), the defendant (in this case, the insurance company) was responsible for paying the plaintiff’s attorney fees. So not only were insurers paying for fraudulent lawsuits, they were also paying for the fraudster’s legal costs. Friedlander notes that the insurance reform bill passed in December 2022 “addresses the two root causes of Florida’s residential insurance crisis — litigation abuse and assignment of benefits (AOB) abuse…Eliminating both is necessary to slow down the mass volume of lawsuits being filed against Florida insurers.” Going forward, assignment of benefits forms are banned for home insurance losses and Florida will no longer operate a one-way attorney fee system.

Roof age

Instead of leaving altogether, some companies are tightening their underwriting restrictions to lessen the risk of these scams. This may be the reason why several companies — including Southern Fidelity, Progressive and Universal — have chosen to continue operations in Florida but have nonrenewed tens of thousands of policies.

However, companies are now prohibited from denying coverage solely based on roof age if the roof is fewer than 15 years old and has a life expectancy of five years at the time the policy is issued. That said, insurers will have to decide if they are comfortable with these restrictions or if they will continue leaving Florida.

Storm risk

Risk will always be a consideration for home insurance companies in Florida. The state’s shape and geographic location mean that it could get hit from either side by a hurricane. Because the peninsula is so thin, even homes in the interior counties aren’t entirely protected.

To make matters worse, fraudulent claims may be more common after severe storms — and storms are not uncommon in the state. Hurricane Ian made landfall on September 28 as a powerful Category 4 storm, causing widespread damage. The damage and financial fallout could push the already-teetering home insurance market into collapse due to increased home repair expenses, including the potential of fraudulent roof claims.

However, although the risk of hurricane damage complicates things, it isn’t what’s driving the market to the brink of collapse. After all, other risky states don’t have this problem. A high likelihood of damage generally means paying a higher premium to offset that risk, but coverage is usually still available. Oklahoma, for example, has the highest average cost of home insurance in the nation at $3,593 per year for $250K dwelling coverage due to the likelihood of tornado damage, but homeowners in the state don’t face the same difficulty finding coverage that Floridians do.

Is anything being done to curb the crisis?

Yes, although the full effects of the measures have yet to be seen. Senate Bill 76 went into effect in July 2021 and included several provisions to curb fraudulent claims causing insurers so much strain. One such provision is aimed at reducing the solicitation tactics that fraudulent contractors often use at the start of a scam. While this legal measure may help solve the problem, Sean Harper, CEO of Kin Insurance, warns that “there will need to be additional action taken to restore the market to health.”

Florida lawmakers met for a special session from May 23 through May 27. The Legislature passed an insurance reform bill that includes several provisions to help slow the spiral of the market. The provisions included setting up the My Safe Florida Home Program, which provides grants to help Florida homeowners strengthen their homes against damage. Additionally, home insurance companies will not be able to deny coverage for homes solely based on roof age if a roof is less than 15 years old and still has five years of useful life left (older roofs may still be denied as they present a high risk of damage). Finally, lawyers will be restricted in the rates they can charge for property insurance claims cases, hopefully discouraging fraudulent lawsuits and decreasing litigation costs.

Update: December Special Session yields promising reform legislation

Additional legislation was signed into law on December 16, 2022. Senate Bill 2-A. The bill has numerous provisions but focuses on one-way attorney fees and the assignment of benefits scam. Friedlander told Bankrate:

“This is the strongest insurance reform package we have ever seen passed in Florida. It shows Florida’s new legislative leaders understand the enormity of the state’s property insurance crisis and are initiating decisive actions to create a path toward stability of the market.”

Doing away with one-way attorney fees and assignment of benefit forms could potentially remove massive financial pressure from insurance companies and reduce the number of fraudulent lawsuits. The combination of actions included in Senate Bill 2-A will hopefully buoy the rapidly-sinking insurers in the Florida market.

However, Friedlander notes that change won’t happen overnight: “…it will take time to see positive impacts of the legislative reform. We expect home insurance rates in Florida to remain high in 2023 due to expenses associated with ongoing litigation, combined with soaring reinsurance rates and double-digit replacement cost increases driven by escalating prices of construction materials and labor.”

In other words, relief may be coming, but it’ll likely take some time for homeowners and insurers to feel it.

Demotech responds to potential rating downgrades

Because many home insurance companies have been hit hard by the rampant and fraudulent litigation, they may no longer be as financially stable as they were. In late July 2022, financial strength rating company Demotech announced it was considering downgrading the financial strength ratings of 27 property insurance companies.

The situation is complex. While these carriers may no longer have the financial strength they used to, downgrading also causes issues. Downgrading financial ratings impacts homeowners with federally-backed mortgages — those from Fannie Mae and Freddie Mac — because these lenders require home insurance companies with Demotech ratings to maintain at least an ‘A’ level. Demotech has not released the names of the companies it is considering downgrading.

“Preliminary evaluations are just that — preliminary,” Demotech President Joe Petrelli told Bankrate. Some of the 27 could retain an ‘A’ or higher rating. But if these downgrades happen, homeowners whose coverage is with an affected company may need to find another insurance carrier in a market where options are already limited or expensive.

While a rating downgrade may present challenges for a company and its insureds, that hardship cannot, and does not, factor into our ratings, which are based on specific data and the objective application of our rating methodology.— Joe PetrelliPresident of Demotech

The Florida OIR established a reinsurance fund through its last-resort insurer, Citizens. This means that if an insurance company’s financial strength rating is downgraded below the ‘A’ level, the downgraded company could purchase coverage from Citizens to back it, similar to a co-signer backing a loan. Reinsurance through Citizens would allow the downgraded insurance company to meet Fannie Mae and Freddie Mac’s requirements. This is important because it would prevent policyholders from being required to find a new property insurer. However, a reinsurance solution further strains Citizens, which is already taking on substantial risk by insuring more policyholders in the state as other insurance companies exit Florida.

On September 9, the Florida legislature approved a $1.5 million plan to search for a financial strength rating company to replace Demotech. The state will hire a consultant to seek out alternatives that may include finding another company or creating a state-backed financial strength rating agency. Petrelli released a statement in response:

“Since 1996 in Florida, Demotech has provided neutral, unbiased ratings to property insurers, among the approximately 50,000 such ratings we have produced across the country. Our review and analysis process has remained consistent throughout this time. Currently, at least four rating organizations acceptable to the government-sponsored mortgage enterprises operate in Florida and countrywide, and a research effort on rating alternatives could be accomplished at no cost to the taxpayers by reviewing existing Freddie Mac and Fannie Mae sellers or servicer guides. Today’s action is an unnecessary response to a problem that does not exist. The reality is that when Hurricane Andrew devastated the state nearly 30 years ago, the rating agencies involved in Florida chose to step away — but Demotech stepped up.”

It remains to be seen if finding another ratings agency will produce meaningful results toward correcting the Florida home insurance crisis. As always, Bankrate continues to monitor the situation.

How to lessen your risk of nonrenewal

If you live in Florida, having a plan could help you lessen your risk of receiving an insurance nonrenewal. There’s nothing you can do to prevent your company from pulling out of the state, but there are steps you can take to make your home as insurable as possible:

Keep your roof updated and in good shape: Inspect your roof regularly and repair minor damage as it happens. If you can afford to, replace your roof before it reaches 15 years of age to lessen the risk of being nonrenewed.

Install wind mitigation features: State law requires Florida home insurance companies to offer discounts for certain wind protection features, such as hurricane straps and other roof-bracing measures. These features lessen the risk of severe damage to your home, thus making your property more attractive to insurers.

Maintain your property: Generally, maintaining your property will make finding insurance coverage easier. Along with checking your roof, also regularly check the rest of the exterior features of your home for damage. You should also make sure no large tree branches or other potential hazards overhang your home, as these could put you at risk of roof damage in a windstorm.

Additionally, there are ways you can lessen the impact of home insurance fraud and help keep companies from having to liquidate. ICA Carter points out that “consumers have the power to help stop contractor fraud by being informed and reporting fraud.”

Know the signs and stay educated: ICA Carter created educational resources called “Demolish Contractor Fraud: Steps to Avoid Falling Victim” that may help homeowners recognize the signs of fraud, stop it before it happens and report it.

Be wary of solicitation: Soliciting business isn’t against the law, but contractors who canvas neighborhoods after storms — and especially those who offer incentives and rebates for an inspection — may be part of a scam. Instead, contact your insurance company if you are concerned your home sustained damage after a storm.

Do not sign an assignment of benefits form: These forms have been banned by Senate Bill 2-A, but keeping an eye out for them as you work with a contractor could still be useful. By keeping control of your policy, you decide if a lawsuit is filed, which vastly cuts down on fraudulent litigation. It’s worth noting that these forms are often buried within otherwise legitimate-looking contracts. Once you’ve signed, the form is legally binding, so it’s important to read everything you are asked to sign. Do not let a contractor simply point out a signature section on paperwork or scroll past the details on a tablet screen. Read the entire document carefully.

Additionally, some companies now offer a discount if you agree to make your policy unassignable. Kin is one such company, and Harper notes that having a high number of unassignable policies has shielded the company from much of the litigation nightmare ensnaring other carriers.

What to do if your home insurance has been canceled

If you’ve received a Florida homeowners insurance cancellation, act quickly. With hurricane season approaching and the insurance market in turmoil, getting another policy could be difficult, but it is possible.

McFaddin recommends that you “work closely with your insurer or insurance agent to see what options may be available to you.” ICA Carter’s advice was similar, advising that “consumers should contact their insurance agency immediately to determine what their options are for homeowners insurance.”

If you’re struggling to find home insurance coverage in Florida, there are still a few companies that may be able to help.

Kin

No home insurance company in Florida is immune to the ripping effects of raging litigation, but Harper notes that his company has “some things that we’re doing that allow us to stay open in Florida when other folks aren’t or are going out of business.” In addition to the bulk of the company’s policies being unassignable, the company also employs a unique system for assessing claim damage.

Harper explains that Kin uses software that monitors weather systems and accurately pinpoints which houses may be damaged. The company can then proactively reach out to homeowners to determine if a claim needs to be filed, thereby cutting out potentially predatory contractors.

It sounds crazy, right, to be an insurance company that is asking our customers for claims? But it actually pays off.— Sean HarperCEO of Kin Insurance

Citizens Property Insurance Corporation

Citizens is often one of the only options for homeowners in many areas of the state. The company has experienced rapid growth due to other carriers leaving the market. In 2018, the company had only 414,000 active policies; by August 2022, that number had ballooned to over 1,000,000. Michael Peltier, the spokesperson for Citizens, told Bankrate that the company is writing 5,000 to 6,000 new policies per week, and that in many parts of the state, Citizens is “the only game in town right now.”

Even so, Peltier says that “we do have underwriting guidelines,” so it may not be an option for all homeowners. Citizens is also affected by the same issues that are plaguing other insurance carriers and have recently raised their rates. Although the company requested a 10.7 percent increase on standard home insurance policies, the Florida OIR approved a 6.4 percent increase. While 6.4 percent is certainly better than 10.7 percent, it’s likely that many Citizens policyholders will still feel the strain of a larger bill. The rate increase will go into effect on September 1.

Additionally, Friedlander warns that, because Citizens is insuring so many of the high-risk homes that other carriers have walked away from, “a major hurricane striking Florida could have devastating effects” on the company and the industry. Offering reinsurance to companies if Demotech does downgrade ratings will add more risk to Citizens if a disaster strikes.

Citizens may get some relief from the December 2022 reform bill, though. Policyholders must now accept private insurance quotes if they are no more than 20 percent higher than Citizens’ quotes. Additionally, Citizens’ rates must be actuarially sound but are now required to be non-competitive with the private insurance market. Finally, Citizens policyholders will be required to carry flood insurance. Rates for a last-resort policy are likely to be higher going forward, but that should theoretically help curb the influx of policies that could drown Citizens entirely.

Update: Slide Insurance takes on some St. Johns and UPC policyholders after insolvency

Since its 2021 inception, Tampa-based company Slide Insurance has embraced taking on books of business from insolvent Florida home insurance companies.

In February of 2022, the Florida OIR announced that Slide would absorb about 147,000 policyholders from St. Johns Insurance Company when it reported its insolvency. In a similar move, approximately 72,000 UPC Insurance policyholders were transferred to Slide when UPC went belly-up in February 2023.

But what is Slide Insurance? Founded by former Heritage Insurance CEO Bruce Lucas, Slide is an insurtech that relies on AI and large data sets for its underwriting models. The company claims this is the edge it needs to thrive in the challenged Florida homeowners insurance market. Slide is rated A (Exceptional) by Demotech.

If you’re one of the many homeowners who have found themselves transferred to Slide, you might be wondering what’s next. According to the company, policyholders have no actions to take — as long as you pay your premiums, there will be no lapse of coverage. Additionally, Slide will notify your mortgage company for escrow purposes (if applicable).

One important thing to note is that Slide will not handle any open UPC claims that occurred before February 1, 2023. Instead, those that need help with an existing UPC claim should contact the UPC claims center directly.

Update: Florida OIR announces Tailrow Insurance Company as newest carrier to enter the Florida home insurance market

In April 2023, the Florida OIR announced that it approved the application for Tailrow Insurance Company, bringing a new carrier into the state.

While Tailrow is yet to be formed (the company has provisions to meet before the OIR will authorize it to do business), this may be a promising first step in stabilizing the market. Bankate’s experts are committed to staying on top of this story and will bring our readers new information as it unfolds.

The bottom line

Florida home insurance has always been complex due to the state’s high risk of storm damage, but the incidence of fraudulent roofing claims has pushed the market to the brink of collapse. The problem may not stay in Florida, either; if other high-risk states like Louisiana and California see an increase in insurance fraud, those markets could begin to degrade. There is hope, though, as measures are put into place to protect companies and policyholders from financial strength rating downgrades, laws are passed that could help curb scams and carriers take a different approach to insuring homes in the Sunshine State. But will these measures be enough to save a market in turmoil?

At the beginning of March, Aria Babu quit her job at a think tank to dedicate herself to something most people have never heard of. Having worked in public policy for several years, the 26-year-old Londoner had come to an alarming realisation about the future of the UK, the world – and the human species.

‘It became clear to me that people wanted more children than they were having,’ Babu says. ‘Considering this is such a massive part of people’s lives, the fact that they were not able to fulfil this want was clearly indicative that something was wrong.’

The new focus of Babu’s career is a philosophy known as pronatalism, literally meaning pro-birth. Its core tenet is deceptively simple: our future depends on having enough children, and yet life in developed countries has become hostile to this basic biological imperative. Linked to the subcultures of rationalism and ‘effective altruism’ (EA), and bolstered by declining birth rates, it has been gaining currency in Silicon Valley and the wider tech industry – especially its more conservative corners.

‘I’ve been in various text threads with technology entrepreneurs who share that view… there are really smart people that have real concern around this,’ says Ben Lamm, a Texas biotech entrepreneur whose company Colossal is developing artificial wombs and other reproductive tech (or ‘reprotech’) that could boost future fertility.

‘We are quite familiar with the pronatalist movement and are supporters of it,’ says Jake Kozloski, the Miami-based co-founder of an AI matchmaking service called Keeper, which aims to address the ‘fertility crisis fueled by a marriage crisis’ by helping clients find the other parent of their future children.

‘I encourage people who are responsible and smart and conscientious to have children, because they’re going to make the future better,’ says Diana Fleischman, a pronatalist psychology professor at the University of New Mexico and consultant for an embryo-selection start-up (she is currently pregnant with her second child).

Easily the most famous person to espouse pronatalist ideas is Elon Musk, the galaxy’s richest human being, who has had 10 children with three different women. ‘If people don’t have more children, civilisation is going to crumble. Mark my words,’ Musk told a business summit in December 2021. He has described population collapse as ‘the biggest danger’ to humanity (exceeding climate change) and warned that Japan, which has one of the lowest birth rates in the world, ‘will eventually cease to exist’.

In an Insider article last November that helped bring the movement to wider attention, 23andMe co-founder Linda Avey acknowledged its influence on the Texan tech scene, while the managing director of an exclusive retreat, Dialog, co-founded by arch-conservative investor and PayPal pioneer Peter Thiel, said population decline was a frequent topic there.

Babu, who hopes to join or create a pronatalist organisation in the UK, says it is still ‘niche’ here but gaining ground on both the ‘swashbuckling intellectual Right’ and the more family-focused and Blue-Labour-tinged segments of the Left.

At the centre of it all are Simone and Malcolm Collins, two 30-something American entrepreneurs turned philosophers – and parents – who say they are only the most outspoken proponents of a belief that many prefer to keep private. In 2021 they founded a ‘non-denominational’ campaign group called Pronatalist.org, under the umbrella of their non-profit Pragmatist Foundation. Buoyed by a $482,000 (£385,000) donation from Jaan Tallinn, an Estonian tech billionaire who funds many rationalist and EA organisations, it is now lobbying governments, meeting business leaders, and seeking partnerships with reprotech companies and fertility clinics.

The Collinses did not coin the word ‘pronatalism’, which has long been used (along with ‘natalism’) to describe government policies aimed at increasing birth rates, or mainstream pro-birth positions such as that of the Catholic Church. Its opposite is ‘anti-natalism’, the idea that it is wrong to bring a new person into the world if they are unlikely to have a good life. Lyman Stone, a natalist demographer and research fellow at the US’s Institute for Family Studies, has described the Collinses’ philosophy as ‘a very unusual subculture’ compared to millions of everyday natalists. Yet it is their version – a secular, paradoxically unorthodox reconstruction of arguably the most traditional view on earth, driven by alarm about a looming population catastrophe – that is prospering among the tech elite.

‘I don’t think it’s appealing to [just] Silicon Valley people,’ Malcolm tells me on a long call from his home in Pennsylvania. ‘It’s more like, anyone who is familiar with modern science and familiar with the statistics is aware that this is an issue, and they are focused on it. The reason why you see Silicon Valley people disproportionately being drawn to this is they’re obsessed with data enough, and wealthy enough, to be looking at things – and who also have enough wealth and power that they’re not afraid of being cancelled.’

The Collinses – Winnie Au

The problem, he concedes, is that falling birth rates are also a common preoccupation of neo-Nazis and other ethno-nationalists, who believe they are being outbred and ‘replaced’ by other races. ‘A lot of alleged concerns about fertility decline are really poorly masked racist ideas about what kinds of people they want on the planet,’ says demographer Bernice Kuang of the UK’s Centre for Population Change.

The Collinses strongly disavow racism and reject the idea that any country’s population should be homogenous. Still, Babu finds that many in the rationalist and EA community, which skews pale and male, are wary of exploring pronatalism – lest they be ‘tarred with the brush of another white man who just wants an Aryan trad-wife’.

Another issue is what you might call the Handmaid’s Tale problem. From Nazi Germany’s motherhood medals to the sprawling brood of infamous, Kansas-based ‘God hates fags’ preacher Fred Phelps, a zeal for large families has often been accompanied by patriarchal gender politics. For liberal Westerners, the idea that we need to have more babies – ‘we’ being a loaded pronoun when not all of us would actually bear them – may conjure images of Margaret Atwood’s Gilead.

Some more illiberal countries are already shifting in this direction. China has begun restricting abortions after decades of forcing them on anyone who already had one child. Russia has revived a Soviet medal for women with 10 or more children. Hungary, where fertility long ago dropped below 2.1 births per year per woman – the ‘replacement rate’ necessary to sustain a population without immigration – has tightened abortion law while offering new tax breaks and incentives for motherhood. Following the end of Roe v Wade in the US, Texas has proposed tax cuts for each additional child, but only if they are born to or adopted by a married heterosexual couple who have never divorced.

But the Collinses contend that this kind of future is exactly what they are trying to prevent. ‘People often compare our group to Handmaid’s Tale-like thinking,’ says Malcolm, ‘and I’m like: excuse me, do you know what happens if we, the voluntary movement, fails…? Cultures will eventually find a way to fix this; how horrifying those mechanisms are depends on whether or not our group finds an ethical way.’ Though they define themselves politically as conservatives – Malcolm invariably votes Republican – they claim to favour LGBT rights and abortion rights and oppose any attempt to pressure those who don’t want children into parenthood.

Instead, they say, their hope is to preserve a ‘diverse’ range of cultures that might otherwise begin to die out within the next 75 to 100 years. They want to build a movement that can support people of all colours and creeds who already want to have large families, but are stymied by society – so that ‘some iteration of something that looks like modern Western civilisation’ can be saved.

‘We are on the Titanic right now,’ says Malcolm. ‘The Titanic is going to hit the iceberg. There is no way around it at this point. Our goal is not to prevent the Titanic from hitting the iceberg; it’s to ready the life rafts.’

It was on the couple’s second date, sitting on a rooftop and gazing out at the nearby woods, that Malcolm first raised the prospect of children. Simone’s response was not enthusiastic.

‘I was very excited to spend my life alone, to never get married, to never have kids,’ she recalls. ‘People would be like, “Do you want to hold the baby?” I was one of those who’s like, “No, you keep it. I will watch that baby from behind glass and be a lot more comfortable.”’

As she says this, her five-month-old daughter Titan Invictus – the couple refuse to give girls feminine names, citing research suggesting they will be taken less seriously – is strapped to her chest, occasionally burbling, while Malcolm has charge of their two sons Torsten, two, and Octavian, three. They live in the leafy suburbs of Philadelphia, balancing parenthood with full-time jobs as co-chief-executives of a travel company, writing books about pronatalism, and their non-profit projects (to which they donated 44 per cent of their post-tax income last year). They project an image of accentuated preppiness, dressing in ultra-crisp country club, business casual when photographers visit, and are effusive and open to the press. Malcolm starts our interview by saying, ‘Absolutely spectacular to meet you!’

The Collins family – Winnie Au

Both dealt with adversity in their own youths. Malcolm, 36, was held by court order in a centre for ‘troubled’ teenagers, where he was told by staff that if he resisted they would simply invent new infractions to keep him locked up. Simone, 35, now needs hormone therapy to menstruate regularly and IVF to conceive a child due to years of anorexia.

Back then, Simone was a textbook anti-natalist. She grew up as the only child of a failed polyamorous marriage among California hippies, where her understanding of a wedding was ‘everyone puts on masks in the forest and there’s a naked sweat lodge’. She was also a ‘mistake baby’, who watched her mother struggle with shelving her career ambitions.

What changed Simone’s mind was not any kind of Stepfordian conversion but a simple promise from Malcolm that she would not have to surrender her career. So it proved. She took no time off during Octavian’s gestation, answered business calls while in labour, and returned to the office five days after his birth. She stays with each child continuously for their first six months, carrying them in a chest harness while working at a treadmill desk, after which Malcolm handles the bulk of child-raising. She finds she gets a productivity bump with each newborn – ‘You’re up every three hours anyway, so why not knock off some emails?’

These personal epiphanies might not have translated into political ones except for Malcolm’s stint as a venture capitalist in South Korea, where the fertility rate is the lowest in the world at 0.8. He was shocked that nobody seemed to regard this as an emergency.

‘If this was an animal species it would be called endangered,’ says Malcolm. ‘We would be freaking out that they are about to go extinct.’ He begins our interview by speaking without interruption for nearly half an hour, incredibly quickly and with frenetic intensity as if chased by the enormity of what is coming.

Virtually every developed nation is now below replacement rate, and the United Nations predicts that the global average will sink below that line around 2056. By 2100 only seven countries are projected to remain above 2.1, mostly in sub-Saharan Africa, meaning developed nations won’t be able to rely on immigration to keep growing.

The impact on actual population will be delayed by decades and hopefully offset by increasing life expectancy, so our species will probably grow through most of the 21st century before holding steady or starting to shrink (estimates vary).

Most demographers do not consider this a crisis, according to Bernice Kuang. ‘In pop culture, there’s so much really alarmist talk about fertility and population implosion, and that just doesn’t really come up in the same way in academia,’ she says, noting that we cannot predict the long-term impact of future ‘reprotech’. Many experts also see overall population decline as a good thing, arguing that it will help prevent or mitigate climate change and other problems.

But pronatalists argue that problems will manifest long before this, as working-age people begin to be outnumbered by older ones. The global economy is predicated on the assumption of continual growth in GDP, which is strongly linked to population growth. ‘If people assume that the economy is going to shrink in future, and shrink indefinitely, then it’s not just a recession – it’s like there’s no point investing in the future,’ says Babu, who defines her politics as economically liberal, feminist, and pro-immigration. ‘If that happens, your pension breaks down because your pension is gambled on the stock market. You withdraw your savings; the government can’t borrow. A lot of these structures just break down.’

Aria Babu – Aria Babu

Take the UK’s current economic doldrums and broken public services, which Babu blames partly on the combination of Britain’s ageing population and the flight of younger immigrants after Brexit. What happens when populations everywhere are ageing or shrinking? One omen is Japan, which is ageing faster than any other nation. A Yale professor called Yusuke Narita, who has become an icon among angry young people, has proposed ‘mass suicide and mass seppuku [ritual disembowelment] of the elderly’ as ‘the only solution’, although he later said that this was merely ‘an abstract metaphor’.

For the Collinses, all of this is only part of the crisis, because the fertility of different cultural groups is not declining uniformly. Research by Pronatalist.org found that higher birth rates are associated with what some psychologists call the ‘Right-wing authoritarian personality’ – or, as Malcolm puts it, ‘an intrinsic dislike and distrust of anybody who is not like them’. That is, says Malcolm, emphatically not his or Simone’s brand of conservatism, which welcomes immigration and wants a pluralistic, multicultural society in which all groups are free to raise their children in their own way of life. By contrast, progressives and environmentalists have fewer children on average, not least because of a widespread despair about climate change among millennials and Gen Z.

There is also emerging evidence that the personality traits thought to undergird political beliefs – such as empathy, risk-taking, and a preference for competition vs cooperation – may be partly inherited. A literature review by New York University and the University of Wisconsin found evidence that political ideology is about 40 per cent genetic. Hence, the Collinses fear that as fertility declines it will not be some racial Other who outbreeds everyone else but each culture’s equivalent of the neo-Nazis. ‘We are literally heading towards global Nazism, but they all hate each other!’ says Malcolm.

What is to be done? ‘Our solution is, uh, we don’t have a solution,’ he admits. He says the only things proven to increase birth rates are poverty and the oppression of women, which are bad and should be stamped out. The only hope is to find those few families that combine liberal, pluralistic politics, such as support for LGBT rights, with high fertility – or create new, hybrid micro-cultures that value both – and help them multiply.

That means creating new educational and childcare institutions, supporting alternative family structures (the nuclear family is historically very unusual, and struggles to support large broods), repealing red tape such as sperm- and egg-freezing regulations, and cutting the cost of fertility treatments.

‘We’re trying to rebuild the high-trust networks that existed before the industrial revolution,’ says Pronatalist.org’s 20-year-old executive director Lillian Tara. ‘Raising children takes a village, and we’re trying to create that village.’ It also means resisting any attempt by what Malcolm calls the ‘woke mind virus’ to assimilate their children into a progressive monoculture.

This is where technology comes in. ‘Many of the groups that we are concerned about disappearing – gay couple couples, lesbian couples – from a traditional organs-bumping-together standpoint, can’t have kids… that are genetically both of theirs,’ says Simone. ‘That certainly dissuades some people from having kids entirely.’ A still-nascent technique called in vitro gametogenesis (IVG), which grows eggs and sperm directly from stem cells, could change this. Cheaper egg freezing and IVF could lighten the trade-off between career and motherhood for women.

Then there are those who struggle with inheritable problems such as depression and schizophrenia. Diana Fleischman says she knows many ‘wonderful people’ who are leery about having children for this reason. Such problems could be mitigated by genetic screening and embryo selection. Titan was born through just such a process, the Collinses tell me, winning out over other embryos that had higher estimated risks of traits such as obesity, migraines and anxiety.

The idea of using birth rates to influence future politics is one many will find alarming. It echoes the American ‘Quiverfull’ movement, which dictates that Christians should breed profusely so that over time society will be stuffed full of good believers.

Malcolm is blunt that some techies are trying to do just that. ‘Silicon Valley people, they’ve done the math, and they actually do want to replace the world with their children,’ he says. ‘They’re like, “Oh yeah, I have eight kids, and if those kids have eight kids, and those kids have eight kids, then at the end my kids will make up the majority of the world’s population… I understand these people’s mindset. They’ve been economically successful… they think they’re better than other people.’ (Musk, he insists, is not of this persuasion.)

Fleischman says she has encountered this too: ‘A lot of this is secret, because it’s just not socially acceptable to say, “I’m going to use my wealth to make as many half-copies of myself as possible. I’m going to photocopy myself into the future.”’

While Musk has been open about his pronatalist beliefs, others are staying quiet to maximise their chance of victory, notes Malcolm. ‘They’re like, “Why are you broadcasting this? We all know this, we can fix this on our own, we don’t need the diversity that you seem pathologically obsessed with”… they’re the people you’re not hearing from.’ Musk did not respond to a request to be interviewed.

If people don’t have more children, civilisation is going to crumble. Mark my words,’ Musk told a business summit in December 2021 – (Apex MediaWire Photo by Trevor Cokley/U.S. Air Force

The Collinses aren’t worried about this, because they think it is doomed to fail. They want to build a durable family culture that their descendants will actually want to be part of, not just ‘spam their genes’, and to help other families with different values do the same. ‘You have an 18-year sales pitch to your kids… and if you fail, well f—k you – your kid’s gonna leave,’ says Simone. ‘The people who carry forward their culture and viewpoints are going to be people who love being parents.’

Even so, this project inherently requires making some judgment on which cultures should prosper in future – and therefore, potentially, which genomes. That rings alarm bells for Emile Torres, a philosopher who studies the history of eugenics and its counterpart, dysgenics – the notion that humanity’s gene pool is slowly becoming somehow worse.

‘Dire warnings of an impending dysgenic catastrophe go back to the latter 19th century, when this idea of degeneration became really widespread in the wake of Darwin,’ Torres says. ‘Biologists were warning that degeneration is imminent, and we need to take seriously the fact that intellectually “less capable” individuals are outbreeding.’ Often this meant poor people, disabled people, non-white people, or other groups lacking the political power to contest their designation as inferior, leading to atrocities such as the Nazi sterilisation regime.

The Collinses – despite using embryo selection – say they reject that kind of eugenics, and Malcolm pours scorn on the ‘pseudoscience’ idea that intelligence or political personality traits differ meaningfully between ethnicities. Rather, he argues that they cluster in much smaller cultural groups such as families or like-minded subcultures. When screening their own embryos, the Collinses did not worry about traits such as autism or ADHD. ‘We don’t think humanity can be perfected, we just want to give our kids the best possible roll of the dice,’ says Simone, who herself is autistic and Jewish.

Still, Torres argues that voluntary, ‘liberal’ eugenics can end up having the same effect as the coercive kind by reinforcing whatever traits are seen as desirable by the prevailing ideology, such as lighter skin, mathematical reasoning or competitiveness. Lyman Stone’s verdict last year was scathing: ‘My policy goal is for people to have the kids they want, but these “pronatalists” would abhor that outcome because it would yield higher fertility rates for people they think shouldn’t breed so much.’

Malcolm says he shares those concerns, which is why he is committed to being almost totally agnostic about which families Pronatalist.org works with. ‘If we act as anything other than a beacon, then we are applying our beliefs about the world to the people we recruit, which goes against our value set,’ he says.

The Collins family – Winnie Au

To sceptics, pronatalism’s appeal in Silicon Valley may simply look like the latest messianic project for a community already convinced that they are the best people to colonise space, conquer death and fix the world’s problems. Yet it speaks to a sense of disquiet that is widely shared. You do not need to fear dysgenic doom to feel that something is fundamentally broken about the way we have and raise children – as many recent or aspiring parents are already aware.

‘In almost every low-fertility country, no one is able to have the number of children they want to have. Even in South Korea, people still want to have two children; they don’t want to have 0.8,’ says Kuang. But far from being an inevitable consequence of progress, she contends that it stems from specific choices we force on to families.

‘The first half of the gender revolution was women attaining educational attainment at parity with men, entering the workforce at parity with men,’ she continues. But the second half remains unfinished, leaving many women caught between mutually incompatible expectations at work versus at home – the classic ‘have it all’ problem. In South Korea, where the new president (a man) has declared that structural sexism is ‘a thing of the past’, a government pamphlet advised expecting mothers to prepare frozen meals for their husbands before giving birth and tie up their hair ‘so that you don’t look dishevelled’ in hospital. ‘Wow, you wonder why women aren’t rushing to sign up for that kind of life?’ laughs Kuang.

Partly of the problem is that middle-class parents are now expected to micromanage their children’s upbringings more intensely than ever before. ‘It seems like in the past six- and seven-year-olds were just allowed to be feral… now it would basically be considered abuse to leave your child alone all day,’ says Babu.

Then there is the cost of housing. ‘How are you going to have two children, even if you desperately wanted to, if you can barely afford a one-bedroom apartment?’ asks Kuang, who would love to have three or four kids if only she could square the mortgage. Babu likewise says becoming a parent would be an easy choice if she knew she could still have a high-flying career and make enough money for a decent home. As it is, she’s torn.

Kuang concedes that no government has yet fixed these problems, but she does believe they are fixable. Although cash bonuses, lump sum payments and restricting abortion have all proven ineffective, she says, robust parental leave for all genders could make a difference. So could high-quality, affordable childcare that is available in adequate supply, and begins as soon as parents need to go back to work.

In the meantime, the Collinses hope to have at least four more babies, unless they are thwarted by complications from repeated C-sections. ‘When I look into the eyes of our children,’ says Simone, ‘and I see all the potential they have… and I think about a world in which they didn’t exist because we thought it was inconvenient? I’m like, I can’t. I can’t not try to have more kids.’

All the hype surrounding TV shows like “Tiny House, Big Living” and “Tiny House Nation” have piqued the interest of people looking for a financially and environmentally sustainable lifestyle. But what looks good on reality TV can be much less appealing in real life — especially if you have children.

A home is generally considered tiny if it’s less than 600 square feet. However, the average tiny home is much smaller — just 225 square feet, according to a 2021 survey by Porch Research.

Tiny homes come in several varieties. At the higher end are traditional stick-built or modular homes constructed on permanent foundations. A more common style is built on a mobile trailer using conventional construction materials. It’s also possible to convert a shed or storage container into a tiny house by using the structure as the home’s shell.

But no matter how you construct your tiny home, you might encounter the same problems with it — so, keep reading to see why you should think twice before springing for that purchase.

The difference between a trend and a fad is staying power. Trends endure and evolve, whereas fads are met with wild enthusiasm for a short time, but then they fizzle.

The tiny-home movement might’ve sprung from the trend toward minimalism and experiential lifestyles, but many proponents dive in without considering the significant challenges inherent in living in a tiny space — suggesting that tiny homes are a fad, not a trend.

The small size of tiny homes doesn’t make them much cheaper to build — in fact, the typical tiny house costs more per square foot than larger houses do, in part because larger construction jobs make for more efficient use of resources.

The average 2,600-square-foot home costs about $190 per square foot to build, according to Fixr, whereas the best-selling home constructed by Tumbleweed Tiny House Company — one of the best-known tiny-house builders in America — costs about $326 per square foot.

3. It Might Be a Home, but It’s Probably Not a House

Many tiny homes are built on trailers, which makes them recreational vehicles. In fact, the Tumbleweed Tiny House Company calls its products “tiny house RVs” and builds its homes according to the Recreational Vehicle Industry Association certification standards. By Tumbleweed Tiny House Company’s own definition, its products are RVs, not houses.

4. Houses — Even Tiny Ones — Must Be Built to Code

Tiny homes built on foundations typically must meet the same code requirements as any other house, but the cost might be disproportionate — and even prohibitive — if you’re working with a bare-bones budget. You might have to prepare the land for construction, pull permits, order inspections and pay to bring utility service to the site.

RyanJLane / Getty Images

5. Many Tiny-Home Owners Aren’t Tiny-Home Dwellers

Owners of tiny homes don’t necessarily live in their houses full time. Often, these owners use their homes as vacation getaways or trade up for larger homes. The challenges that come with living in a tiny home aren’t so challenging if you’re only there for a few nights per year.

kate_sept2004 / Getty Images

6. Millennials Might Regret Their Home Purchase

According to the “Real Estate Witch 2023 Millennial Home Buyer Survey,” Millennials’ biggest homebuying regret is paying too much interest (22%), which could make a case for going tiny. But almost as many (18%) regret not anticipating future needs — a regret that’s likely much more prevalent among tiny-home buyers.

A tiny home that works for individuals might not work for couples. And what works for a couple might not accommodate a baby and the supplies that come along with having one. Even bringing a pet into the mix can overcrowd your tiny space.

While some cities have loosened zoning restrictions to accommodate tiny homes, most cities don’t allow tiny homes on wheels to be parked in residential yards or used as permanent residences without the appropriate permits. You’ll have to research local codes and ordinances before you make any decisions, or park your tiny home in an RV park or other designated area.

Tiny living takes a lot of work. You’ll have to go grocery shopping more often, pick up mail from a post office box and do frequent small loads of laundry in a compact washing machine. You might also have to empty out a composting toilet, climb in and out of a sleeping loft and grapple with multifunction furniture that needs to be opened or closed — or folded and unfolded — every time you use it.

Tiny living looks like a simple lifestyle at first glance, but it can actually be rather chaotic. Tiny houses often have low ceilings and tight transition spaces that require residents to constantly duck and squeeze as they navigate their surroundings, prepare meals, take showers and climb into bed. Even eating takeout becomes a chore when you lack adequate dining space.

AleksandarNakic / iStock.com

11. The Cramped Space Wears On Your Mental Health

An overcrowded home has been linked to increased stress and anxiety in families, likely due to lack of privacy and disrupted sleep. Children might also find it difficult to locate a quiet place to read or complete schoolwork in such close quarters.

Unless you’re allowed to park your tiny home in someone’s backyard, you’ll have to find a place to put it — and that costs money. You can purchase land if you have enough savings or lease a lot — perhaps in an RV park or manufactured home community — for a fixed price per month.

Even if zoning laws allow you to build or park a tiny home, you’re not necessarily out of the woods. Those laws might also mandate the minimum size of the lot that your home sits on — typically 1,000 square feet. Considering that lots cost anywhere from about $6 per square foot in Mississippi to over $110 per square foot in Hawaii, according to Angi, lot requirements could interfere with your dreams of constructing your home on a small budget.

State and local governments have their own building codes for homes built on permanent foundations. Permanent tiny homes often don’t meet those standards, so you’ll need to check the tiny-house ordinances for the specific city you’re living in.

A tiny home built on a trailer isn’t real estate, even if you own the land that it’s parked on. Tiny homes on wheels are personal property, and like other personal property — such as cars and RVs — they depreciate over time. Real estate, on the other hand, usually appreciates over time.

In the event that you want or need to sell your tiny home, finding a buyer won’t be easy. Tiny homeownership has more barriers to entry than traditional homeownership — there simply aren’t as many people willing to live in 400 or fewer square feet.