GOP Lawmaker’s Wild Claim About Those Who ‘Hate Homosexuals’ Causes Literal Jaw-Drop

Ed Mazza – May 3, 2023

Fox News Flips Over ‘Woke’ Legos

The right-wing network has added another new enemy to its list — the Lego toy company.

There was a jaw-dropping moment on the floor of the Florida House of Representatives this week after a Republican lawmaker’s comment about who really hates the LGBTQ+ community.

“ISIS, the Taliban and al Qaeda. Those are the folks who discriminate,” state Rep. Jeff Holcomb said Monday. “Our terrorist enemies hate homosexuals more than we do.”

It’s not clear if he misspoke or intended to say it like that, but he was speaking in support of a bill that urges Congress to prohibit “woke social engineering and experimentation” that are “eroding” the military.

The implication that Republicans hate the gay community ― but terrorists hate them even more ― led to gasps in the audience, while Democratic Rep. Kelly Skidmore’s jaw literally dropped:

Florida GOP Representative Jeff Holcomb says the quiet part out loud on the House floor today.

“Our terrorist enemies hate homosexuals MORE THAN WE DO.”

‘Older generations are so confused’: A young woman on TikTok says Gen Z, Millennials don’t share the same work ethic as Boomers — 3 reasons why she might be onto something

Vishesh Raisinghani – May 3, 2023

Generational grumble is old as time itself.

There’s probably a cave painting about how the younger generation had ruined the hunter-gatherer economy with their “fancy agriculture.” Since then, every successive generation has found a new medium to express their disappointment with ‘them young’uns.’

A recent example comes from the comment section on TikTok, which recently erupted when a young lady explained why Gen Z and Millennials don’t exactly share the same values regarding work.

“Older generations are so confused about why we don’t want to work hard anymore or prioritize our careers,” Demi Kotsoris said in the clip “We know how short life is now.”

Kotsoris goes on to explain that the pandemic and greater access to information have reshaped the perspective of younger generations and made them question whether work should be the center of their lives.

Of course, the response was heated. “This mindset is so [‘you only live once’] that you will regret those decisions later,” says one comment on Kotsoris’ video.

“People are just SELFISH & LAZY NOW,” says another.

But the replies may have missed the point of the video. Here’s why Kotsoris’ message resonates with so many younger workers and why her experience highlights some deeper truths about modern work.

Work isn’t as rewarding anymore

For Baby Boomers, there were clear rewards for working hard. Putting in an average amount of effort allowed a typical worker to buy a nice home, raise children comfortably and travel the world. In the 1980s, the average home price was just four or five times the median income. Now, it’s closer to 7.5 times.

Having a college degree was also far more rare in the 80s. Now, nearly everyone in the job market has a degree so its value has been eroded. Meanwhile, the dollar has been eroded too. Wages haven’t kept up with inflation for decades, so an hour of work today isn’t worth as much as an hour of work in the 80s.

Upward mobility has declined too. A person born in a middle-class family in the 1940s was 93% likely to outearn their parents by the age of 30. For those born in the 1990s, that rate is just 45%.

Some Boomers could beat the odds and create generational wealth by investing in stocks. However, even that is not as easy as it used to be. The S&P 500 was trading at around 10 times its earnings during the 1980s. It’s now trading in the low-20s.

The relationship with corporations has changed

The employee-employer relationship has also changed since the 80s. Defined-benefit pension plans are nearly extinct. A major corporation that went public before the 1970s was 92% likely to survive the next five years. By the early 2000s, the rate had dropped to 63%.

Unions have also declined, which means workers now have far less bargaining power than their parents.

All these factors have made younger workers question the value of company loyalty and lifelong careers.

The pandemic altered perspective

The global pandemic may also have shifted work culture

This is true across generations because the crisis triggered a retirement boom too. Meanwhile, younger workers saw how short life can be, and how easily their lifestyle can be disrupted by a global crisis like a pandemic or climate change. A study by Deloitte found that Gen Z and Millennials are more likely to prioritize work-life balance, flexible work arrangements, and purposeful work.

The pandemic highlighted that remote work is a viable option for many companies. In fact, a survey by Buffer found that 98% of remote workers would like to continue working remotely at least some of the time for the rest of their careers.

The warning is in effect for Northeast and Central Florida from noon to 7 p.m. In some locations, the warning is in effect until 8 p.m., according to the National Weather Service.

Low humidity, breezy winds and critically dry conditions prompted the warning.

Winds of 15 mph are expected to be out of the west today, with gusts up to 25 mph. Relative humidity is forecast to be 20 percent to 30 percent.

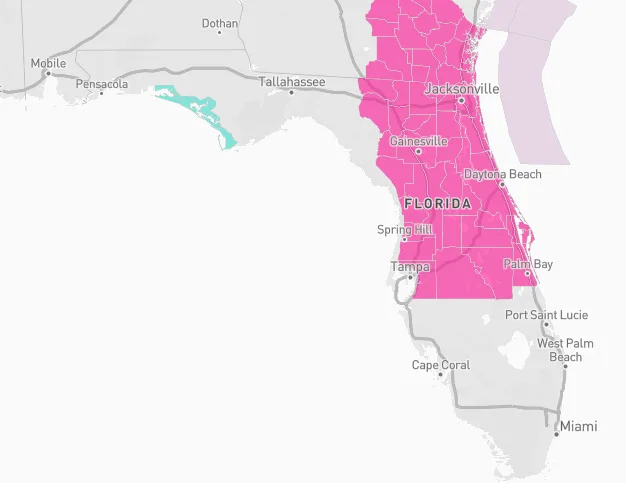

Much of Florida is under a red flag warning May 3, 2023.

A red flag warning means warm temperatures, very low humidity, and stronger winds are expected to combine to produce an increased risk of fire danger, according to the National Weather Service.

Conditions also can cause reignition of any smoldering fires started by recent lightning strikes.

What are the dangers with a red flag warning?

Wildfires can grow quickly under these conditions.

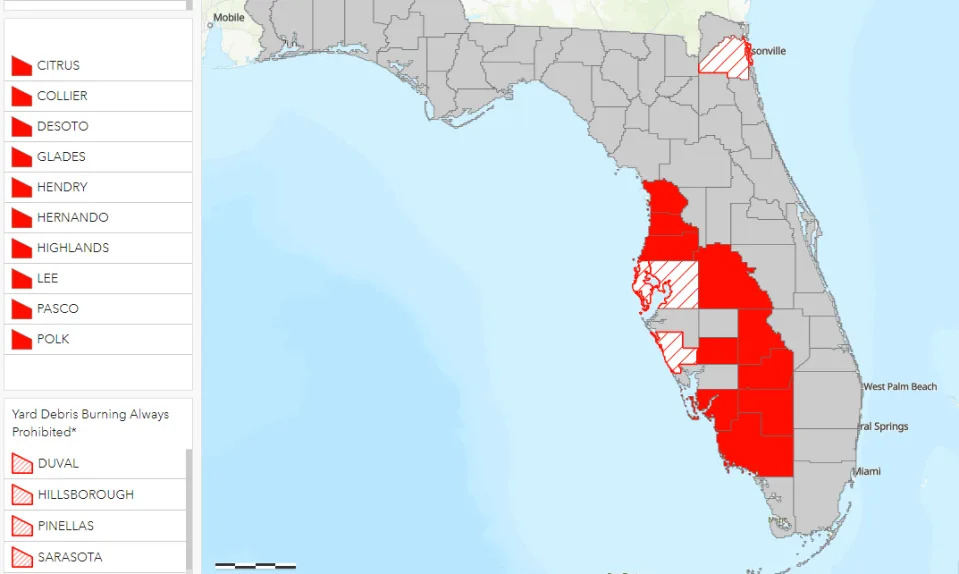

What Florida counties are under a burn ban?

Conditions in Florida prompted a red flag warning for much of the state May 3, 2023. Burn bans in effect.

The Florida Forest Service reports the following counties are under a burn ban as of May 1:

Citrus

Collier

Desoto

Glades

Hendry

Hernando

Highlands

Lee

Pasco

Polk

Burning of yard debris is prohibited year-round under county ordinance in these locations:

Duval

Hillsborough

Pinellas

Sarasota

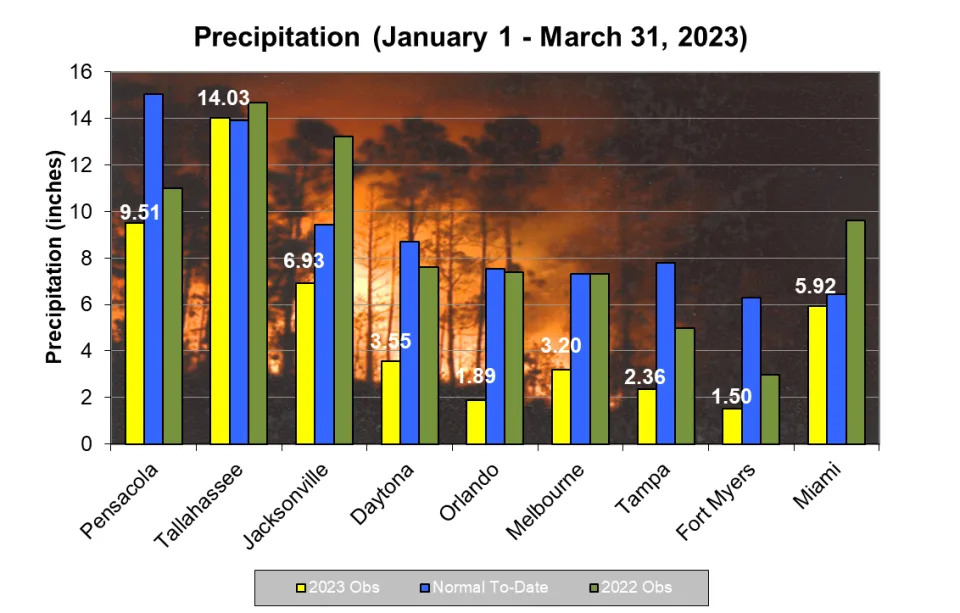

How dry is it in Florida?

Florida rainfall around the state from Jan. 1 through March 31, 2023.

As La Niña continues to make itself felt, for the southeastern U.S., that includes a dry and warm winter and a potentially active wildfire season for Florida, according to the Florida Forest Service.

A combination of above-average temperatures and below-average precipitation was in the forecast throughout all North Florida through March.

There may be good news on the horizon: The drought coverage and intensity may have peaked across Florida in recent past weeks, according to the Climate Prediction Center.

What should you do when under a red flag warning?

If you are allowed to burn in your area, all burn barrels must be covered with a weighted metal cover, with holes no larger than 3/4 of an inch.

Do not throw cigarettes or matches out of a moving vehicle. They may ignite dry grass on the side of the road and become a wildfire.

Extinguish all outdoor fires properly. Drown fires with plenty of water and stir to make sure everything is cold to the touch. Dunk charcoal in water until cold. Do not throw live charcoal on the ground and leave it.

Never leave a fire unattended. Sparks or embers can blow into leaves or grass, ignite a fire, and quickly spread.

Where are active wildfires in Florida?

There are 42 active fires covering more than 5,000 acres currently across the state. The Florida Forest Service maintains a map showing the location, size and percentage contained of current wildfires.

‘Poor people are not stupid’: I grew up in poverty, earned $14 an hour, and inherited $150,000. Here’s what I have learned from my windfall.

Quentin Fottrell – May 3, 2023

‘When I open my accounts and see how they are growing it really fills me with a sense of pride and determination.’

‘My tiny house has been one of the greatest decisions I’ve ever made, and has truly changed my whole mindset on what makes me happy.’ MARKETWATCH

In September 2018, this woman from Texas, then 36, wrote to the Moneyist to ask how she should invest her windfall — over $150,000. It was small by some people’s standards, but it was life-changing to her. She didn’t have a college degree, said she would never earn more than $30,000 a year, and worked full-time for $15 an hour, in addition to a part-time job at $10 an hour. She paid $1,050 a month in rent.

She paid off her car, and bought a “tiny home,” which she owns free and clear, she wrote in an update a year later. She deposited $70,000 in a high-yield online savings account. She topped up her retirement portfolio and invested $30,000 into emerging markets. She maxed out her IRA and invested $10,000 between very safe dividend stocks and ETFs. She also spent $7,000 on dental work in Mexico.

And today? Five years after her first letter, she has updated MarketWatch readers on her progress, and what she learned from this experience:

Dear Moneyist,

There are a lot more Americans making less than $50,000 a year than there are those who make more. I feel like we aren’t really represented in the financial-advice world. I’d love to see more columns helping people to invest $25-$100 when they can. It’s empowering to invest. I might never be a Warren Buffet, but when I open my accounts and see how they are growing it really fills me with a sense of pride and determination.

As to how I’m doing? Beautifully. I hate to say it but the pandemic was a blessing to me personally. I feel terrible saying that because of the loss and devastation so many others suffered and are still suffering because of it, but for me, the pandemic opened up a world of possibilities. A job opportunity landed in my lap because of the shutdown, and I’m making almost $4,000 a month now after taxes.

Yes, me! I’ve never made so much money before (outside of the inheritance I received). I am still frugal and live off of about $1,800 a month, and that includes health insurance, long-term disability insurance, full-coverage car insurance, and pet insurance! Everything else goes to savings and investments. I won’t say what it is I’m doing because it might identify me, but I will say it is a job that allows me to be happy every second I’m “working.”

My tiny house has been one of the greatest decisions I’ve ever made, and has truly changed my whole mindset on what makes me happy. As I’ve lived in it I’ve altered certain parts of the design to be more efficient, and I can honestly say I intend to live tiny until some mobility issue — hopefully age-related and not an accident of some kind! — forces me back into a more conventional dwelling. Tiny living forces you to be mindful. Not only of your space, but also of yourself, and how you live in your space. It might sound strange to hear, but living tiny has truly made me a better person and improved my quality of life in ways other than financial.

I would like to address some of the comments I read in response to your previous article on my letter. While most were truly supportive others were coming from a place of judgment and condescension. I’d like to thank everyone who wished me well, and for them to know that their words meant a lot to me. That people took time out of their day to read about me and wish me well was uplifting. I send them all virtual hugs and hope each and everyone is happy and healthy.

However, I’d also like to address some of the comments that were less encouraging. Several people insisted that my letter was obviously fake because of how well I wrote, and that someone with my education level could not possibly be in the financial situation I’m in. I was less hurt by this attitude as I was utterly astounded by it. That people genuinely believe the educated cannot struggle financially just floored me.

‘There are more ‘poor’ Americans than there are ‘rich’ Americans, and we are not stupid or lazy. We’re trying to make it work.’

Poor people are not stupid. We’re not illiterate country bumpkins struggling to figure out how to work a computer. We’re the nurse that lives down the street with two roommates to be able to afford rent. We’re the teachers still living with their parents because they can’t find enough roommates to qualify for an apartment. We’re the cops working at Home Depot on the side trying to save up for a baby. We’re the lawyers doing Uber just to afford student-loan payments. There are more “poor” Americans than there are “rich” Americans, and we are not stupid or lazy. We’re trying to make it work — usually by having 2-3 jobs.

There is a financial crisis in this country. I believe it comes from unchecked capitalism. When corporations are allowed to buy up single-dwelling homes and drastically raise rents, and banks/lending institutions are allowed to prey on people with obscenely high interest rates, you foster an environment of exploitation. Our society allows for the targeting of young people before they even graduate high school. Credit-card companies and college-loan institutions begin preying on people as soon as they hit 18. If their parents are financially illiterate, and considering most public schools rarely teach financial literacy, too many young people start out life with insane amounts of debt. Additionally, wages have not kept pace with the cost of living in this country, and you have a lot of educated “poor” people.

I just could not believe those comments that insisted this story was fake because I was too educated to be poor. Then I was mad. Mad because that stereotype is what prevents a lot of change from taking place. Nothing is ever going to get better if we keep thinking the worst of each other.

Anyway, I again want to thank you for thinking of me and sharing my story. Hopefully it helped more people. As I said before, investing is truly empowering. I didn’t know that before, but I know it now, and I wish it for many more Americans.

Sincerely,

Not Quite As Low Income, But I’m Still A Couponing Lady

Dear Not Quite As Low Income,

Thank you for your insightful and eloquent letter. Your words and story continue to inspire me, and I hope will inspire many others out there in America who never had a head start in life and/or continue to face financial struggles. I wish you the best of everything in your life, and I hope more good things continue to happen to you.

This woman was told her mortgage was paid off: 10 years later, she received a foreclosure notice in the mail. She decided to fight.

Aarthi Swaminathan – May 2, 2023

Mortgages originated in the early 2000’s and largely forgotten are now being pursued by debt collectors. Government officials are concerned.

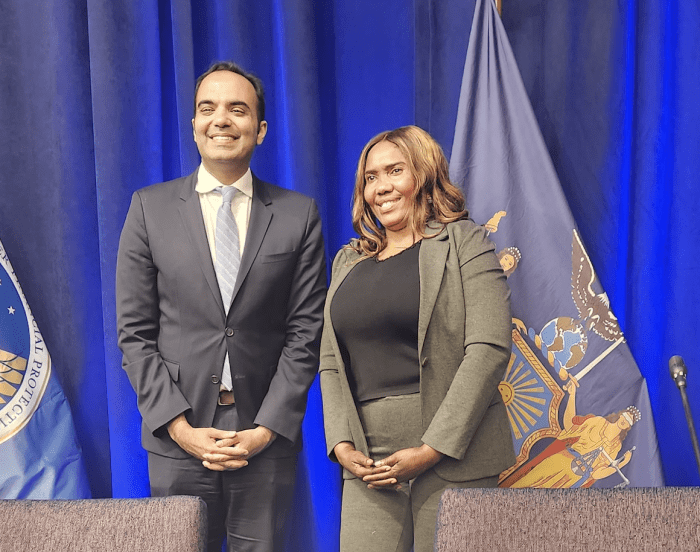

Rohit Chopra, director of the Consumer Financial Protection Bureau, stands beside homeowner Rose Prophete during a field hearing in Brooklyn, N.Y. PHOTO: LEGAL SERVICES NYC

Rose Prophete bought her home in Canarsie, Brooklyn, N.Y. in May 2005. She thought she had paid off her loans until recently, when a company approached her about a debt she thought she had settled a long time ago.

The company expected Prophete to pay up over $130,000, or face foreclosure.

When refinancing her mortgage on the home, Prophete had split her mortgage into two. Prophete said she had been erroneously told that her second mortgage was paid off. That debt, having laid dormant for years, was now being pursued by a debt-collection firm.

Prophete is one of 13 plaintiffs in a 2021 federal lawsuit against the firm, and she recently testified at a field hearing into “zombie debts” held by the Consumer Financial Protection Bureau, a government agency responsible for consumer protection in the financial-services sector.

The CFPB last week announced that it was issuing legal guidance for debt collectors trying to collect on mortgages that were long considered forgiven by borrowers, who in particular had no notices or statements sent over a decade about outstanding debt.

‘This is really frustrating — I don’t want to lose my home.’— Rose Prophete, who bought her home in Brooklyn, N.Y. in May 2005

The federal agency said that a debt collector “who brings or threatens to bring a state-court foreclosure action to collect a time-barred mortgage debt may violate the Fair Debt Collection Practices Act.” Time-barred refers to debt whose statute of limitations has run out.

“Debt collectors do not get to claim ignorance of the law or ignorance of the debt’s age,” Rohit Chopra, director of the CFPB, said during the hearing. “If the statute of limitations has expired, taking legal action threatening to bring a suit of foreclosure may be illegal no matter what the debt collector claims to have known. This is the law.”

Prophete, a Haitian immigrant and a hospital technician, said during the CFPB hearing that she had worked three jobs to afford the two-family Brooklyn home, on top of taking care of small children.

According to the lawsuit, a little more than a year after they completed the purchase, the broker who arranged the financing suggested she refinance the mortgage to lower her monthly payments. She agreed to refinance her mortgage into two, as the broker told her that this “financing structure would be the most financially advantageous to her,” per the filing. The first loan was for $504,000 and the second for $63,000 with an interest rate of 9%.

‘Debt collectors do not get to claim ignorance of the law or ignorance of the debt’s age.’— Rohit Chopra, director of the CFPB, speaking about the Fair Debt Collection Practices Act

After a couple of years, she received a note from her first lender that the second loan was fulfilled — that she didn’t need to pay for it. She said she didn’t receive any statements for the second mortgage, so she focused on paying off her first one, the lawsuit said.

She said she never heard back from the mortgage servicer, until over a decade later, in March 2021, when she received a foreclosure notice in the mail. The creditor was attempting to collect on payments due from Jan. 1, 2009 to the date of filing in 2021. The payments had ballooned from $63,000 to over $130,000, according to the lawsuit.

“This is really frustrating — I don’t want to lose my home,” Prophete said during the field hearing.

New York Attorney General Leticia James, who also spoke during the hearing, said that debt-collection firms were engaged in “predatory practices” to “rob individuals of the equity in their home.”

Debt buyers were acquiring these mortgages “often for pennies on the dollar,” James said, and they were now suing homeowners and “seeking to exploit rising housing values by reviving the long-dormant zombie debt.”

“I find this practice predatory and abusive and an affront to the American dream of sustainable home ownership,” she added. “I will fight this despicable practice.”

Cancer-causing toxins are in shampoos, body lotions, and cleaning products. Here’s what experts want you to know

Robin Dodson, Ruthann Rudel, Megan R. Schwarzman, The Conversation – May 2, 2023

Getty Images

The big idea

Consumer products released more than 5,000 tons of chemicals in 2020 inside California homes and workplaces that are known to cause cancer, adversely affect sexual function and fertility in adults or harm developing fetuses, according to our newly published study.

We found that many household products like shampoos, body lotions, cleaners and mothballs release toxic volatile organic compounds, or VOCs, into indoor air. In addition, we identified toxic VOCs that are prevalent in products heavily used by workers on the job, such as cleaning fluids, adhesives, paint removers and nail polish. However, gaps in laws that govern ingredient disclosure mean that neither consumers nor workers generally know what is in the products they use.

For this study we analyzed data from the California Air Resources Board (CARB), which tracks VOCs released from consumer products in an effort to reduce smog. The agency periodically surveys companies that sell products in California, collecting information on concentrations of VOCs used in everything from hair spray to windshield wiper fluid.

We cross-referenced the most recent data with a list of chemicals identified as carcinogens or reproductive/developmental toxicants under California’s right-to-know law, Proposition 65. This measure, enacted in 1986, requires businesses to notify Californians about significant exposure to chemicals that are known to cause cancer, birth defects or other reproductive harms.

We found 33 toxic VOCs present in consumer products. Over 100 consumer products covered by the CARB contain VOCs listed under Prop 65.

Of these, we identified 30 product types and 11 chemicals that we see as high priorities for either reformulation with safer alternatives or regulatory action because of the chemicals’ high toxicity and widespread use.

Why it matters

Our study identifies consumer products containing carcinogens and reproductive and developmental toxicants that are widely used at home and in the workplace. Consumers have limited information about these products’ ingredients.

We also found that people are likely co-exposed to many hazardous chemicals together as mixtures through use of many different products, which often contain many chemicals of health concern. For example, janitors might use a combination of general cleaners, degreasers, detergents and other maintenance products. This could expose them to more than 20 different Prop 65-listed VOCs.

Similarly, people experience aggregate exposures to the same chemical from multiple sources. Methanol, which is listed under Prop 65 for developmental toxicity, was found in 58 product categories. Diethanolamine, a chemical frequently used in products like shampoos that are creamy or foamy, appeared in 40 different product categories. Canada and the European Union prohibit its use in cosmetics because it can react with other ingredients to form chemicals that may cause cancer.

Some chemicals, such as N-methyl-2-pyrrolidone and ethylene gylcol, are listed under Prop 65 because they are reproductive or developmental toxicants. Yet they appeared widely in goods such as personal care products, cleansers and art supplies that are routinely used by children or people who are pregnant.

Our findings could help state and federal agencies strengthen chemical regulations. We identified five chemicals – cumene, 1,3-dichloropropene, diethanolamine, ethylene oxide and styrene – as high-priority targets for risk evaluation and management under the Toxic Substances Control Act by the U.S. Environmental Protection Agency.

What still isn’t known

Our analysis of the CARB data on volatile toxicants does not paint a complete picture. Many toxic chemicals, such as lead, PFAS and bisphenol A (BPA), don’t have to be reported to the Air Resources Board because they are not volatile, meaning that they don’t readily turn from liquid to gas at room temperature.

In addition, we were not able to identify specific products of concern because the agency aggregates data over whole categories of products.

What other research is being done

Studies have shown that women generally use more cosmetic, personal care and cleaning products than men, so they are likely to be more highly exposed to harmful chemicals in these categories. Further, women working in settings like nail salons may be exposed from products used both personally and professionally.

Ultimately, a right-to-know law like Prop 65 can only go so far in addressing toxics in products. We’ve found in other research that some manufacturers do choose to reformulate their products to avoid Prop 65 chemicals, rather than having to warn customers about toxic ingredients.

But Prop 65 does not ban or restrict any chemicals, and there is no requirement for manufacturers to choose safer substitutes. We believe our new analysis points to the need for national action that ensures consumers and workers alike have safer products.

Florida’s insurance crisis: 2 special sessions, little help | Commentary

Scott Maxwell, Orlando Sentinel – May 2, 2023

For years, Florida lawmakers ignored a looming insurance crisis.

Then, with rates skyrocketing and companies fleeing the state, they scrambled to call not one, but two special sessions, vowing to help.

Well, my wife and I saw what the Legislature’s version of help looks like a few months ago when our insurance bill jumped from $4,000 to $7,000.

Any more “help “like that and we’ll be eating cat food.

In reality, we’ll be just fine. But a growing number of Floridians are facing bills they can barely afford as prices skyrocket throughout the state.

The Insurance Information Institute predicted increases of 40% throughout Florida this year. Some companies have requested 60% hikes. And scores of Floridians are still being dropped by their carriers while the state-run Citizens Property Insurance keeps bloating.

This is an undeniable, mounting mess.

So once again, GOP legislators – who have spent the better part of the past two years waging culture wars – have cobbled together another insurance bill.

But if you’re counting on this lowering your rates, bad news: It will not.

That’s not my take. It’s the take of former GOP Sen. Jeff Brandes – one of the few lawmakers who repeatedly warned his colleagues to take action years ago and was largely ignored.

“Nothing in this bill lowers rates,” Brandes, who now runs the Florida Policy Project, said this week. “Nothing in this bill encourages more companies to come.”

Brandes and I have differing views on some aspects of reform – particularly as it relates to the transparency measures and regulations that subsidized insurance companies should face.

But we agree on three key things:

1. Despite years of yapping about fraud claims driving up costs and rates, Florida lawmakers have never cracked down on bad actors in any meaningful fashion.

2. The solutions they’re talking about now aren’t going to do much, if anything, to bring down rates.

3. Any meaningful solution – in a state like ours that’s basically a bullseye for hurricanes and increasingly at risk of flooding – is going to involve a boatload of public money.

Brandes and I may have varied thoughts on how that money should be spent. But the reality is that this problem – where the state-run insurance company is now covering millions of Floridians at increasingly high rates – requires a major investment and serious policy reform.

And that’s not good news for a Legislature that specializes in divisive bumper-sticker priorities – dragging Disney, fuming about drag queens and decrying wokeism.

When it comes to hard, serious policy work, they are either unwilling or incapable of getting the job done. At least when it comes to insurance.

A clear example of that is fraud. For years, lawmakers have blamed fraudulent claims for driving up insurance costs and driving companies out of the state. But they haven’t done squat from an enforcement standpoint.

“If you want talent in the Office of Insurance Regulation – which should be one of the most talented in the state – you have to pay for it,” Brandes said.

That seems obvious. If your city had a rash of burglaries, you’d beef up your burglary patrol. But Florida politicians have whined about fraud without ever dedicating serious resources to exposing, punishing and stopping it.

If they can set up a statewide election-crime police force to deal with fever-dream problems, you’d think they’d beef up their insurance team to deal with an actual financial nightmare.

But to really bring down prices, we need more competition among providers. Or we need to invest more in Citizens – and basically accept that a giant, costly state-run insurance company is the only way we’re going to be able to cover everyone in a state that’s both storm-ravaged and low-wage.

Few people really want that second option. Certainly not Brandes. But many of us aren’t super keen either on just handing over tax dollars to an industry with a track record of hosing its policy holders.

Just a few weeks ago, the Washington Post published a maddening investigative report that found Florida insurance companies were financially victimizing hurricane survivors by gutting their claims and payments – sometimes by as much as 90% of what the companies’ own adjusters said the homeowners were due. The piece featured an adjuster who said one insurance company took his report – which estimated $200,000 in valid claims for one home – and whittled it down to just $27,000 without his knowledge or consent.

Brandes prefers offering companies incentives to write Florida policies. That may be worth exploring – with a lot of checks and balances added in.

But here’s the bottom line: Either scenario – majorly subsidizing private industries or growing/transforming Citizens into something like a Florida version of Medicare for homeowners – is painful. They’re both costly, politically unpopular and involve a lot of hard work.

Unfortunately, most Florida politicians don’t want to do hard work or make unpopular moves. So they just keep screaming about critical race theory and transgender athletes. And while they scream, your rates keep rising.

I think we’re heading toward a pain point – where even the Floridians who used to laugh at the culture wars are going to stop laughing once they realize they can barely afford to stay in their homes. That may be when they start finally putting people in office who are more interested in solving problems than creating them.

U.S. Supreme Court to examine whistleblower claims against financial firms in UBS case

Daniel Wiessner – May 1, 2023

FILE PHOTO: U.S. Supreme Court building in Washington

(Reuters) -The U.S. Supreme Court on Monday agreed to examine how difficult it should be for financial whistleblowers to win retaliation lawsuits against their employers as the justices took up a long-running case involving Switzerland’s UBS Group AG.

The justices will hear an appeal by Trevor Murray, a former UBS bond strategist, of a lower court’s decision to throw out his 2021 lawsuit that accused the company of unlawfully firing him for refusing to publish misleading research reports and complaining about being pressured to do so.

The appeal involves a technical but important issue – whether whistleblowers who sue their employers for retaliation under the federal Sarbanes-Oxley Act must prove that companies acted with “retaliatory intent.”

The New York-based 2nd U.S. Circuit Court of Appeals last year decided that Murray was required to meet that bar and failed, creating a split with four other federal appeals courts. Those courts have said that defendants in Sarbanes-Oxley cases can raise the lack of intent as a defense, but that plaintiffs do not have to prove employers acted with intent.

A Supreme Court ruling in favor of UBS could significantly curtail financial whistleblower lawsuits because it is often difficult for plaintiffs to prove a defendant’s motives.

Robert Herbst, a lawyer for Murray, said the 2nd Circuit decision ignored the text of the whistleblower law, adding that he looked forward to arguing the case before the Supreme Court.

A UBS spokesperson said, “We expect the court will uphold the 2nd Circuit’s decision.”

Murray, who worked in UBS’s mortgage securitization unit, accused UBS officials of pressuring him to issue skewed and bullish research on commercial mortgage-backed securities in order to support the bank’s trading and underwriting operations. He has said he was fired in 2012 about two months after complaining to supervisors and despite receiving excellent performance reviews.

UBS has denied wrongdoing and said Murray’s termination was part of a cost-cutting campaign that eliminated thousands of jobs.

The Sarbanes-Oxley Act was adopted in 2002 and created enhanced accounting standards for publicly traded U.S. companies after a series of accounting scandals, along with new legal protections for employees who report illegal conduct.

The Supreme Court is due to hear the case in its next term, which begins in October.

(Reporting by Daniel Wiessner in Albany, New York; Editing by Will Dunham)

Hotel housekeeping jobs have fallen by 102,000 during the pandemic. What happened?

Levi Sumagaysay – May 1, 2023

‘Before the pandemic, I never had a problem with getting hours,’ one housekeeper told MarketWatch

The number of hotel housekeepers has fallen since the onset of the pandemic. GETTY IMAGES/ISTOCKPHOTO

As some U.S. hotels hung on to practices they adopted during the early stages of the coronavirus pandemic — such as eliminating daily room cleanings — the number of hotel housekeepers fell by more than 102,000 last year from prepandemic levels, new data show.

The total number of hotel housekeeping jobs as of May 2022 was 364,990, a 22% decline from the total of 467,270 such positions during the same period in 2019, according to numbers released last week by the Bureau of Labor Statistics.

Unions representing hotel service workers feared this would happen, and had warned a couple of years ago of such a decline. Since then, they have worked to restore or retain routine daily housekeeping in hotel rooms around the country. In some places that actually began requiring daily cleanings during the pandemic, unions are pushing to make those rules permanent.

In Las Vegas, the Culinary Workers Union is opposing legislation that would repeal daily-cleaning requirements as it tries to protect the jobs of thousands of hotel housekeepers in a travel destination known as the entertainment capital of the world.

“Prior to the pandemic, it was standard that you paid a pretty penny for a nice room and you got service,” Ted Pappageorge, the secretary-treasurer for Culinary Workers Union Local 226, said in an interview. “You didn’t have to chase someone down the hall” to ask for towels or for trash to be taken out of your hotel room, he said.

“Now room rates are higher, 30% or more, [and hotels are] expecting guests to do without,” Pappageorge added.

The biggest U.S.-based hotel chains have reported that their average daily room rates have risen since 2019. Hilton Worldwide Holdings Inc. HLT, +1.05% reported last week when it released first-quarter earnings that its revenue per available room was 8% higher than during the same period in 2019. Marriott International Inc. MAR, +4.98% and Hyatt Hotels Corp. H, +3.06% report earnings this week.

But according to their fourth-quarter earnings filings with the Securities and Exchange Commission, Marriott’s revenue per available room was up 4.6% over the same period in 2019 and Hyatt’s for that same period rose 2.4%.

Hilton, Marriott and Hyatt did not respond to requests for comment about their daily housekeeping policies. All three hotel chains in earnings updates have reported increasing their numbers of properties. At least one, Marriott, mentioned in its November report that it was dealing with “industry-wide labor shortages” that made it challenging to hire or re-hire for certain positions.

The Las Vegas–based Culinary Workers Union and its members also said less-frequent cleanings could be a safety issue, because housekeepers don’t know what they might find in a room that hasn’t had a hotel staff member inside it in several days. In addition, having fewer people around in massive hotels could mean no one within earshot during attempted assaults on housekeepers, they said.

Housekeepers who spoke with MarketWatch said getting rid of daily cleanings or requiring guests to ask for daily cleanings means not just fewer jobs, but harder work for those who have managed to keep their jobs.

Proponents of the Nevada legislation include the Henderson Chamber of Commerce, which said in a recent letter to state lawmakers that “eliminating health requirements on businesses that are no longer needed is another step in ensuring our economy returns to pre-pandemic levels.”

The general counsel of Wynn Resorts Ltd. WYNN, -2.08% assured the state legislature in a letter that the hotel chain “will continue to clean our hotel rooms daily to maintain our Forbes Five Star designation,” though it does not believe a mandate by law is necessary and supports “the rescission of the statutory requirement which imposes upon resort operators unprecedented business operational requirements.”

Housekeepers who spoke with MarketWatch said doiing away with daily cleanings or requiring guests to ask for daily cleanings means not just fewer jobs, but harder work for those who have managed to keep their jobs.

Nely Reinante, a housekeeper at Hilton Hawaiian Village who told MarketWatch two years ago that she was waiting to return to work full-time because daily cleanings weren’t happening at the time, worked with the union to help restore routine daily cleanings at her hotel. Among other things, they passed out leaflets to explain the situation to guests.

“Our guests are happier now that there is no trash or dirty linens or towels in the hallway,” Reinante said in a recent interview with MarketWatch. She is back to work full time, she said, though some of her colleagues quit because they couldn’t afford to wait around for full-time work.

Reinante said that compared with a couple years ago, she “can breathe lighter now” because it’s easier to handle rooms that are cleaned daily — and she’s not worried about not getting enough hours.

“Guests can support housekeepers by always asking for daily housekeeping when they check in,” Unite Here International President D. Taylor said in an emailed statement. The union and its affiliates, such as the Culinary Workers Union local in Nevada, have worked to restore automatic daily housekeeping in many major cities around the country, Unite Here said.

A housekeeper in the Boston area told MarketWatch earlier this year that some guests thought they were helping housekeepers by opting out of daily cleanings. In reality, the housekeeper said, some staff weren’t being assigned enough shifts.

“Before the pandemic, I never had a problem with getting hours,” said Josefina Lopez, who works at the Element Boston Seaport District and was only getting a couple of days of work a week at the beginning of this year. Lopez also hurt her shoulder because she was having to spend more time cleaning rooms and her work had become harder, she said at the time.

Since then, though, Lopez has resumed full-time work, according to her union.

Taylor, the Unite Here president, said he is proud of restoring automatic daily housekeeping at many union hotels. “But now you’ve got a patchwork effect where some hotels have full service automatically and others don’t, even if they’re part of the same brand,” he said. “That’s not fair to guests. And it only widens the gap between the union standard and nonunion working conditions.”

Treasury Secretary Janet Yellen speaks during a press conference at the Treasury Department in Washington, on April 11, 2023. (Yuri Gripas/The New York Times)

WASHINGTON — A vote by House Republicans last week to lift the nation’s debt limit in exchange for deep spending cuts was the first step in what is likely to be a protracted battle over raising or suspending the borrowing cap to avoid defaulting on United States debt.

But while Republicans and President Joe Biden and his fellow Democrats are gearing up for a fight, a key question is beginning to sow unease in Washington and on Wall Street: How much time is there to strike a deal?

The United States technically hit its $31.4 trillion debt limit in January, forcing the Treasury Department to employ accounting maneuvers known as extraordinary measures to allow the government to keep paying its bills, including payments to bondholders who own government debt. Treasury Secretary Janet Yellen said at the time that her powers to delay a default — in which the United States fails to make its payments on time — could be exhausted by early June. She cautioned, however, that the estimate came with considerable uncertainty.

With June now just a few weeks away, uncertainty around the timing of when the United States will run out of cash — what’s known as the X-date — remains, and determining the true deadline could have huge consequences for the country.

Tax receipts will be key to the X-date.

Determining the X-date depends on a complex set of factors, but ultimately what matters most is how much money the government spends and how much it takes in through taxes and other revenue.

The Bipartisan Policy Center, which tracks federal revenues, projected in February that lawmakers would need to raise or suspend the debt limit sometime between summer and early fall to avoid a default. The specific date would largely depend on how quickly tax revenues are coming into the government’s coffers.

There are signs that 2022 tax receipts are trickling in too slowly for comfort. Economists at Wells Fargo wrote in a note to clients last week that because tax collections appear to be weaker than expected, there is a chance the X-date could be as soon as early June. However, they continue to believe early August is the most likely default deadline.

“A low but not insignificant probability of a U.S. default is still very concerning, and we would think the last thing Treasury officials want is an X-date that sneaks up on Congress,” they wrote.

Tax day payments are still arriving. Goldman Sachs economists projected last week that by the second week of June, the Treasury Department could have around $60 billion of cash remaining, which would allow the government to keep making its payments until late July.

Natural disasters could fuel a debt disaster.

There is a surprising factor that could cause the X-date to arrive sooner: the weather. Severe storms, flooding and mudslides in California, Alabama and Georgia this year prompted the IRS to push the April 18 filing deadlines in dozens of counties to October.

The IRS said this year that, because of the storms, individuals and businesses in the affected areas could file their returns late. They were also given more time to make contributions to retirement and health savings accounts.

Farmers, who often file their tax returns by March 1, also have received a reprieve until Oct. 16, and estimated payments that normally would have been made in January were allowed to be pushed back to that date.

It is not clear how much tax revenue has been delayed by the storms, but the extensions have given the Treasury Department less wiggle room to keep paying the bills.

An update could come this week.

The Treasury Department is expected to send a letter to Congress in the coming days with a more precise estimate of when it could start running out of cash. It could also lay out new measures intended to stave off a default. This year, Yellen announced that she would redeem some existing investments and suspend new investments in the Civil Service Retirement and Disability Fund and the Postal Service Retiree Health Benefits Fund.

In a speech last week, Yellen warned that a default would have real consequences for the economy.

“Household payments on mortgages, auto loans and credit cards would rise,” Yellen said in remarks to the Sacramento Metropolitan Chamber of Commerce in California. “And American businesses would see credit markets deteriorate.”

She added, “On top of that, it is unlikely that the federal government would be able to issue payments to millions of Americans, including our military families and seniors who rely on Social Security.”

Here’s what the X-date means for negotiations.

As the X-date approaches, it will put more pressure on lawmakers to take action.

Analysts at Beacon Policy Advisors predicted that if a default could really happen as soon as June, that would increase the likelihood that Congress will pass a short-term suspension of the debt limit through October. If the X-date is expected to hit in July, that might compel lawmakers to file legislation by early May so they have sufficient time to deal with procedural obstacles in Congress.

Although markets have broadly remained calm about the prospect of a default, there are some signs that investors are becoming nervous.

They have sold government bonds that mature in three months — around the time policymakers have said the United States could run out of cash — and snapped up bonds with just one month until they are repaid.

The cost of insuring existing bond holdings against the possibility that the United States will default on its debts has also risen sharply. Still, analysts say the market reaction would need to be much more pronounced to force a fast deal.

“This has caused some heartburn among policymakers but not enough to move the negotiating needle in a meaningful way,” the Beacon analysts wrote. “There needs to be a bigger market response and a more definitive X-date to get negotiations going in full.”

That has yet to happen, however. While Biden has indicated he is open to talking with House Speaker Kevin McCarthy about ways to get the nation’s fiscal situation on a better track, the two have yet to schedule a meeting after the House passage last week.