MarketWatch – In One Chart

HELOCs are back. Cash-strapped borrowers are tapping into a $33 trillion pile of home equity.

Joy Wiltermuth – June 26, 2023

Banks hold most HELOCs

Goodbye pandemic refi cash-outs. Hello HELOCs?

Home-equity lines of credit (HELOCs) and second-lien mortgages have been staging a notable comeback as U.S. homeowners look for liquidity and ways to monetize the pandemic surge in home prices, according to BofA Global.

It used to be that borrowers sitting on an estimated $33 trillion pile of equity built up in their homes could simply refinance and pull out cash, until the Federal Reserve’s rapid rate hikes began squelching the option.

Now, with mortgage rates above 6%, and the Fed penciling in two more rate hikes in 2023, cash-strapped homeowners have been seeking out alternatives to extract cash from their properties.

While cash-out refinances tumbled 83% in the fourth quarter of 2022 from a year before, HELOCs rose 7% and home-equity loans grew 31%, according to the latest TransUnion data.

“Borrower demand remains high, particularly given household budgets have been pressured by rising food and energy costs,” a BofA Global credit strategy team led by Pratik Gupta’s, wrote in a weekly client note.

Risky loans to subprime borrowers and home equity products helped precipitate the 2007-2008 global financial crisis and the era’s wave of devastating home foreclosures.

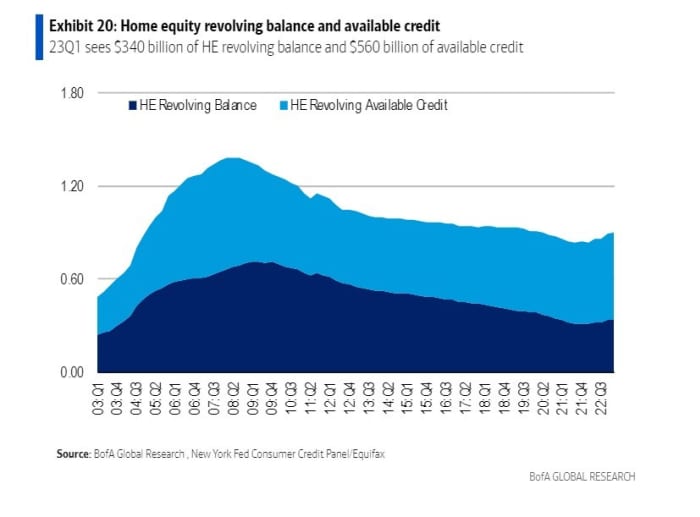

At the time, households had more than $1.2 trillion of home equity revolving and available credit (see chart), whereas the figure was closer to $900 billion in the first quarter of this year.

The pandemic saw home prices surge, giving a big boost to home equity levels. The Urban Institute pegged home equity in the U.S. at $33 trillion as of May, up from a post-2008 peak of about $15 trillion.

BofA analysts argued this time home equity products look different, with roughly $17 trillion of tappable equity across 117 million U.S. homeowners, and most borrowers having high credit scores and low rates.

“The vast majority of that — $14 trillion — is from the cohort of homeowners who own their homes free & clear,” Gupta’s team wrote.

Another $1.6 trillion of equity could be available from Freddie Mac and Fannie Mae borrowers, according to his team, which pegged an estimated 94% of all outstanding U.S. first-lien home mortgages now below 4% rates.

Major banks own the bulk of home equity balances (see chart), led by Bank of America Corp. BAC, +1.23%, PNC Bank PNC, +0.57%, Wells Fargo, WFC, -0.05%, JPMorgan Chase JPM, +0.24% and Citizens CFG, +0.35%, according to the team, which notes several other major banks appear to have hit pause on their programs.

A smaller portion of HELOCs and second-lien mortgages have been securitized, or packaged up and sold as bond deals, while nonbank lenders have been offering the products as well.

Related: The economy was supposed to cave in by now. It hasn’t — and GDP is set to rise again.