This state is requiring every new home to be built with money-saving, energy-efficient heat pumps: ‘The right choice’

Jill Ettinger – October 9, 2023

Starting this summer, every new house or apartment built in the state of Washington will be required to use money-saving, energy-efficient heat pumps for heating and cooling.

The decision came last November when the Washington State Building Code Council voted in favor of the mandate, making it one of the strongest building codes in the country for energy-efficient heat pumps.

Electric heat pumps are two to four times more energy efficient than gas heaters, which means they can help you cut down your electricity bill dramatically.

Another reason they’re being lauded is because they don’t run on methane, a potent gas that traps heat in our atmosphere and causes our planet to overheat. Methane is also linked to a number of human health issues, including respiratory illness, memory loss, and heart disease.

The Council voted for the heat pumps following a 2021 state law that requires 45% in greenhouse gas pollution reductions by 2030 and 95% by 2050, compared with 1990 levels. The state is also required to increase energy efficiency in buildings by 70% by 2031.

“The State Building Code Council made the right choice for Washingtonians,” Rachel Koller, managing director of the green-building alliance Shift Zero, said in a statement. “From an economic, equity and sustainability perspective, it makes sense to build efficient, electric homes right from the start.”

An influx of transplants to Washington in recent years has led to a 50% increase in planet-overheating gas pollution from buildings between 1990 and 2015 — the fastest-growing source in the state.

Across the country, lawmakers are making decisions like this to help move their municipalities away from dirty-energy-based heating systems. More than 90 cities and counties in the U.S. now have similar measures in place.

“It’s an exciting step forward toward meeting our goal to reduce greenhouse gases in our state,” Katy Sheehan, a council member who voted in favor of the heat pump mandate told Spokane’s Spokesman-Review. “I’m really happy that we did it.”

These ‘self-sustaining’ luxury homes take just 6 weeks to construct — and buying one could literally earn you money

Laurelle Stelle – October 9, 2023

A construction company called S2A Modular is providing a range of luxury prefabricated homes in as little as six weeks — and each is designed to produce its own free electricity.

For most homeowners, the power bill is a major monthly expense. According to the U.S. Energy Information Administration, the average U.S. residence used 10,632 kilowatt hours in 2021. More than half of that energy went to heating and cooling, with the rest going to lights, appliances, and electronics.

But S2A Modular co-founders John Rowland and Brian Kuzdas envision a world where you don’t pay power companies for electricity — they pay you.

Enter #GreenLuxHome: S2A Modular’s electrically self-sustaining houses. The homes are designed to reach “Net-Zero,” meaning that they supply at least as much energy to the local power grid as they draw from it.

“With your home connected to the grid as a backup power source, soon enough, you won’t only eliminate energy bills,” says the company’s website, “utility companies may eventually write you checks for your home having contributed energy.”

The site goes on to say that the homes use Tesla Powerwall batteries and FreeVolt PV Graf solar panels to provide enough power not just to supply the needs of the household, but to charge electric cars as well.

This approach is an obvious money-saver for homeowners, but it’s also great for the environment. Solar power doesn’t produce heat-trapping gases, unlike electricity generated from burning coal or gas, so it contributes much less to rising global temperatures.

Meanwhile, S2A Modular’s homes are designed for quality and value. The company offers a selection of 35 gorgeous floor plans and the option to design your own, all using high-quality materials and built-in smart features.

Once you choose the design that suits you, S2A Modular says the house will be completely ready for move-in in six weeks.

As the company says, “You save time. You save money. You save energy. And your home has immediately higher long-term value than a traditional ‘site-built’ home.”

It’s true NJ, your commute stinks. Census data says it’s third-worst in U.S.

Manahil Ahmad – October 4, 2023

Recent data on travel times in the United States has found that New Jersey has the third-longest average time people spend getting to work.

The U.S Census shared these results, highlighting the tough daily journeys faced by people in the state of New Jersey due to crowded roads and public transportation.

The study looked at data from big cities all over the country. It showed that in New Jersey, people spend about 30.3 minutes on an average going to work each day. This is almost five minutes more than the national average, showing just how tough commuting is in the Garden State.

Being very close to major cities like New York City and Philadelphia makes things harder, as many folks cross state borders for work, making the traffic situation even worse.

Supreme Court Weighs Fate of Consumer Agency That Vexes Banks, Riles GOP

Greg Stohr – October 2, 2023

Thirteen years after a Democratic-controlled Congress created the CFPB to regulate mortgages and other consumer-finance products, the high court on Tuesday will weigh a novel constitutional argument that the bureau’s supporters say could leave it decimated.

The clash will shape the future of an agency that critics see as the ultimate symbol of an unaccountable and overreaching federal bureaucracy – but that backers including President Joe Biden’s administration say has provided crucial safeguards and an independent check against corporate power in the years since the 2008 financial crisis.

“The CFPB is under attack because it’s good at what it does,” Senator Elizabeth Warren, the Massachusetts Democrat who spearheaded the bureau’s creation, said last week.

The justices, who open their new term Monday, are reviewing a ruling that said the agency’s funding system violates a constitutional provision requiring a congressional appropriation for government spending. The CFPB isn’t subject to the year-to-year congressional appropriation process and instead draws as much money as it needs – up to a cap it has never hit – from the Federal Reserve. In fiscal 2022, the agency received $641.5 million in funding, short of its $734 million cap.

“It’s not about the merits of CFPB,” said Michael Pepson, a lawyer with the conservative Americans for Prosperity Foundation. “It’s about ensuring that Congress doesn’t shirk its duties by passing off its exclusive funding authority to unelected officials.”

The case comes at a time when the CFPB under Biden-appointed Director Rohit Chopra is taking an especially aggressive tack. The agency has sought to stamp out abuses in the mortgage-lending market, scrutinize the use of artificial intelligence in credit underwriting and rein in so-called junk fees, a catch-all term that include charges for bounced checks and late credit-card payments.

The bureau last year reached a $3.7 billion settlement with Wells Fargo & Co. to resolve allegations that it mistreated its customers for years by illegally repossessing cars, bungling record-keeping on payments and improperly charging fees and interest. Beyond banks, the CFPB under Biden has sought to probe “buy-now-pay-later” firms and penalize student lending servicers and credit reporting agencies.

Since the CFPB was created in 2010, its enforcement actions have returned $20.2 billion in compensation, principal reductions, canceled debts, and other relief to consumers, agency spokesperson Samuel Gilford said.

The activity is only fueling longstanding Republican complaints that the agency is too powerful. At a hearing in June, GOP Representative Andy Ogles of Tennessee told Chopra the bureau “should die a painful death.”

Mortgage Worries

Although the high court case centers on a never-enforced payday-lending rule, the impact is potentially far broader. In urging the justices to take up the case, the bureau said the ruling from the 5th US Circuit Court of Appeals cast a legal cloud over every action the agency has taken since its creation, providing an argument for re-opening even long-finalized rules and enforcement cases.

That’s a worry shared in part by the mortgage-banking industry, which filed a brief urging the court to limit any ruling against the CFPB. The bureau has issued dozens of rules affecting consumer mortgages and the industry has invested billions of dollars toward compliance, according to three trade groups led by the Mortgage Bankers Association.

A decision calling those rules into question “could set off a wave of challenges and the housing market could descend into chaos, to the detriment of all mortgage borrowers,” the groups argued.

The payday-lending trade group pressing the challenge, the Community Financial Services Association, calls those concerns overblown. Judges have a variety of tools to prevent disruption of the mortgage market, including the six-year statute of limitations that applies to CFPB rules, the group says.

“Lacking any viable legal argument, the bureau resorts to fear-mongering about significant disruption if all the CFPB’s past actions are vacated,” the trade group argued. “But the bureau grossly exaggerates the effects and implications of setting aside this rule.”

Delay Suggested

At a minimum, a decision striking down the payday-lending rule could provide a potent new argument for companies currently battling the CFPB, according to Bloomberg Intelligence analyst Elliot Stein. Navient Corp., which is fighting a complaint over its student-loan servicing practices, could have an especially strong case because it has already raised the issue in its defense, Stein said.

Some industry groups – including the US Chamber of Commerce and the American Bankers Association – have suggested the court could take the unusual step of ruling against the agency but delaying the decision’s effective date to give Congress time to set up a different funding system.

The 5th Circuit ruling marked the first time a federal appeals court had ever used the appropriations clause to strike down part of a federal statute. The Supreme Court has never interpreted the clause as a check on Congress, so far invoking it only as a limitation on the executive branch.

The case is part of a Supreme Court term that could put new constraints on federal administrative agencies. The justices are also considering restricting the use of in-house judges to handle cases at the Securities and Exchange Commission. And the court has agreed to revisit an important 1984 ruling that gives agencies latitude in interpreting ambiguous federal statutes.

The Supreme Court in 2020 gave the president broad power to fire the CFPB’s director, striking down job protections Congress had enacted. At the same time, the court stopped short of abolishing the agency altogether, as critics had sought.

The case is Consumer Financial Protection Bureau v. Community Financial Services Association, 22-448.

Democrats tried to protect the CFPB from politics. The Supreme Court may blow up that plan.

Katy O’Donnell – October 2, 2023

Manuel Balce Ceneta/AP Photo

Democrats who created the Consumer Financial Protection Bureau a decade ago thought they could shield the agency from political pressure by funding it through the Federal Reserve instead of Congress.

That decision, which drew condemnation from GOP lawmakers and has helped make the regulator a lightning rod for attacks ever since, is facing its biggest test Tuesday when the Supreme Court hears arguments on its constitutionality.

The case is highly anticipated since it could not only result in curbing the agency’s power and throwing its rules into question but potentially affect other regulators throughout the government — including the Fed and the FDIC — that are also not funded by annual congressional spending bills.

“The CFPB has returned $17 billion directly to Americans cheated by financial institutions,” Sen. Elizabeth Warren (D-Mass.) told POLITICO. “If the Supreme Court disregards over a century of legal precedent, it risks undermining banking regulators safeguarding our economy, as well as Social Security and Medicare.”

Warren, who is credited with conceiving the agency that was created in the wake of the 2008 financial crisis before she became a senator, said the CFPB’s political independence was critical to its formation. Republicans and financial industry critics, many of whom have opposed the bureau since its inception, argue that the funding scheme allows the agency to escape accountability.

Many Democrats see the case as part of a broad-based attack on the regulatory state by Republicans eager to bring challenges before the Supreme Court, whose conservative majority has proved willing to curtail the power of agencies.

In a 2022 ruling limiting the Environmental Protection Agency’s authority to regulate greenhouse gases, the high court’s six GOP-appointed justices invoked the so-called major questions doctrine, saying that agencies like the EPA need congressional approval before “asserting highly consequential power.” The court has also taken up a case this term challenging the constitutionality of the Securities and Exchange Commission’s in-house enforcement proceedings.

The CFPB was created by the Dodd-Frank Act, the landmark 2010 law that rewrote the rules of finance. The funding mechanism set up by Obama-era Democrats allows the bureau to request the amount of money it needs each year from the Fed, which, in turn, is funded by fees it levies on financial institutions and interest on the securities it holds. The CFPB automatically receives the requested amount, subject to a cap set by Congress.

Among the options the Supreme Court has when it makes its ruling, probably next year, is kicking the matter back to Congress to overhaul the way the bureau is financed — a move that would open the door for other reforms to the agency in an election year.

The case was brought by small-dollar lenders challenging a 2017 CFPB rule restricting their activity. An appellate court ruled last year that the current funding system violates the Constitution’s separation of powers doctrine.

The court scrapped the 2017 rule on the grounds that the CFPB was unconstitutionally funded when it adopted the regulation. The ruling held that the agency’s self-determined budget drawn from an agency that is itself not funded by appropriations marked a “double insulation from Congress’ purse strings,” a unique setup even among financial regulators.

The government maintains that Congress’s decision to authorize the Fed to fund the agency up to a fixed level amounts to “a standing, capped lump-sum appropriation,” as Solicitor General Elizabeth Prelogar wrote in an August brief.

Counsel for the payday lender groups, meanwhile, argued that “Congress does not possess unfettered discretion to authorize executive spending, let alone the power to cede virtually unfettered discretion to an agency to determine the size of its own purse in perpetuity,” in their brief to the high court.

If the Supreme Court does decide the funding stream is unconstitutional, the government is urging the justices to “sever” the funding provision from the rest of the law that created the agency.

“A decision invalidating the CFPB’s past actions would be deeply destabilizing” and “threaten profound disruption for consumers, regulated businesses, and the nation’s financial markets,” Prelogar said in the brief.

Housing industry representatives have also called on the high court to preserve existing CFPB regulations. They warned of “potentially catastrophic consequences that a decision drawing those rules into doubt could have on the mortgage and real-estate markets,” in an amicus brief submitted by three of the industry’s most powerful trade groups.

The Chamber of Commerce and nine other industry groups, meanwhile, urged the court to “avoid disruptions in consumer financial markets” in their own amicus brief. But the groups, which include the major banking trades, also stated that they “believe they are entitled to” the invalidation of CFPB actions they have challenged in pending lawsuits related to the agency’s funding mechanism. They also said CFPB “enforcement actions should be paused” until Congress resolves its funding.

Court watchers say wholesale invalidation of past CFPB actions is a remote possibility.

“Nobody wants a remedy where they throw every regulation out the window, and I doubt very much if they would do that,” said Alan Kaplinsky, former chair of the consumer financial services group at Ballard Spahr. “If they get to the point where they’ve got to decide the remedy, I think the conservatives and the liberals on that court would prefer to kick the ball over to Congress and let them try to deal with that.”’

The Supreme Court has already ruled that “the Dodd-Frank Act contains an express severability clause” in a 2020 decision holding that another part of the CFPB’s structure, a single director who could only be fired for cause, violated the separation of powers. While that decision eroded some of the bureau’s political insulation, separating out the removal clause from the rest of the law preserved the agency.

Both bureau backers and critics say a key question is whether a ruling against the agency could apply only to the CFPB and not to other regulators with independent funding.

“I think philosophically there are going to be five to six votes that probably would like to decide against the CFPB,” Kaplinsky said. “What they’re not going to want to do is decide the case and in doing that put a big cloud over the constitutionality of the Fed, FDIC and [the Office of the Comptroller of the Currency] — that would be a horrendous result. I don’t think any of them would want that, it would create economic chaos.”

The scope of the season’s impact, while minimal, was exacerbated by the scalding summer conditions and multiple heat records in a slew of categories.

Thunderstorms were hard to come by this year. Rainfall totals for the monsoon season, which ends Sept. 30, will likely result in the driest-ever summer season at Phoenix Sky Harbor International Airport, where the National Weather Service records the official figure. The rain gauge there posted just 0.15 of an inch, less than half the total of 1924, previously the driest with 0.35 of an inch.

Some areas did fare better, primarily in the East Valley and Cave Creek, where some gauges snagged upward of 4 inches, but the spotty season will still place Maricopa County on the infamous dry list behind 2020’s “Nonsoon.”

Ultimately, this lack of storms helped fuel the full effect of triple-digit temperatures and the sweltering sun to be felt across the state.

In fact, each of the three branches of the National Weather Service — Flagstaff, Phoenix and Tucson — recorded Julys that surpassed the month in years prior, posting their hottest-ever totals.

Flagstaff sees hottest monsoon season on record; Tucson and Phoenix hottest-ever Julys

Climate summary data from the weather service’s website highlights the month’s ferocity. In the Phoenix area, for example, average high temperatures for July were 114.7 degrees, more than eight degrees above the recorded norm between the years 1991-2020.

The average mean temperature was 102.7 degrees, about seven degrees higher than the recorded norm. The most revealing stat was for warm-lows, as nights in Phoenix averaged 90.8 degrees, more than six degrees north of the month’s typical mean.

For Tucson and Flagstaff, climate reports echo a similar song. Tucson posted its hottest July, with an average monthly temperature of 94.2, six degrees hotter than normal. Flagstaff witnessed its warmest July, with a 4.7-degree temperature spike above its typical mark, bringing the overall average figure for the month to 71.4 degrees.

Flagstaff is on pace for its warmest monsoon season on record by just 0.2 degrees, surpassing the number one spot set in 1980.

Rainfall totals shallow compared to recent years

Total precipitation for 2023’s monsoon, recorded at Phoenix Sky Harbor, Flagstaff Pulliam and Tucson International airports, varied across the board:

Flagstaff: 4.24 inches

Tucson: 4.73 inches

Phoenix: 0.15 of an inch

As a whole, the deviation from the norm for Tucson is not that negative.

A typical season usually produces around 5.7 inches of rain for Tucson’s airport, coming mainly in July and August. This was mirrored in 2023, as the prime months brought 2 and 2.39 inches, respectively, making up for a zero in the June column and a lackluster September

Tucson held close to its 2022 mark as well, coming just 0.20 of an inch from eclipsing that year’s total.

In Flagstaff and Phoenix, things get a lot less pretty.

At the high country’s airport, 2023’s accumulation of 4.24 inches puts it well below its average of 7.68. The year was also dwarfed in comparison to 2022 (10.63 inches) and 2021 (10.90 inches).

In Phoenix, Sky Harbor caught an abysmal 0.15 of an inch of rain this season, easily placing it as the driest on record, pushing out 1924 at 0.35 of an inch. Usually, Sky Harbor gets around 2.43 inches of rain during the season.

When compared even to 2020’s “Nonsoon,” a total that both Tucson and Flagstaff handily exceeded, Phoenix’s 2023 comes nowhere close. Sky Harbor got exactly 1 inch of rain that year, according to NWS statistics.

Overall for Arizona, precipitation in 2023 was more in line with typical seasons than that of 2020 and 2021.

“I would say as far as precipitation patterns, it was more typical because of the variability,” NOAA Warning Coordination Meteorologist Kenneth Drozd told The Arizona Republic. “(In) 2022, there were more places that were above normal than below normal, but it was still pretty mixed. Kind of like this year, there are more places that are below normal than above normal, but it still varies quite a bit depending on where you’re at.”

In 2020 and 2021, Drozd said, conditions were “unique” because of their widespread consistencies, with 2020 being so dry and 2021 being much wetter.

Maricopa County on pace to be wetter than 2020

While Sky Habor couldn’t catch a break, Arizona’s most populous county as a whole is set to end the monsoon season in a better position.

According to data from the Maricopa County Flood Control District, the county posted wetter numbers than it did in 2020, in large part due to healthier amounts falling in Cave Creek, Wickenburg, Apache Junction and portions of the East Valley.

Throughout Maricopa County, totals from data stretching back 108 days from the season’s Saturday endpoint bounce around from lows in central Phoenix at 0.39 of an inch to upward of four inches in parts of Cave Creek.

A notable area that performed the best in the county was near rural Crown King north of the Valley, where there were spots receiving nearly eight inches during the storm span.

“In general, the closer to the mountains you are, the more rain you’re going to receive during monsoon because the storms form over them,” National Weather Service Phoenix office meteorologist Mark O’Malley told The Republic. “That just became exacerbated this year where the areas of south Phoenix through Laveen, down through Avondale and Goodyear, some areas didn’t even receive a tenth of an inch.”

According to O’Malley, the lack of storms this season was primarily due to the weather pattern setting up with strong high pressure over southern Arizona, bringing hotter temperatures and lackluster storms.

“The weather pattern was set up to where it favored the heat and the storms were more removed from the area, more frequently,” O’Malley said.

SRP: 3 monsoons touched down in the Valley in 2023

According to data from Salt River Project, three major monsoon storms hit metro Phoenix in 2023: on July 26, Aug. 31 and Sept. 12.

These storms left their marks, too, with SRP reporting estimated outage numbers at the height of each storm:

July 26: 50,000 customers out of power

Aug. 31: 71,000 customers out of power

Sept. 12: 39,000 customers out of power

APS customers were affected as well, with the company reporting approximate outages during peak storm hours:

July 26: 7,750 customers without power

Aug. 31: 18,000 customers without power

Sept. 12: 11,000 customers without power

Each event brought its own force, bringing down power lines, overturning planes, destroying mobile homes and uprooting trees. While par for the course during the season, rainfall totals certainly weren’t.

For July 26, chunks of the storm covered the greater Phoenix area into Scottsdale and swaths of the East Valley, with downtown Phoenix only registering 0.04 of an inch of rain. Paradise Valley and Apache Junction received as much as one full inch during the duration of the storm.

On Aug. 31, more portions of Maricopa County got involved but with far less rain. Only two areas throughout the metro saw upward of a half inch. Much of the rain that fell did so in the Cave Creek and New River areas, ranging from 1.45 to 3 inches through the course of the storm.

A storm on Sept. 12 produced the best results for the Valley, with multiple areas getting over the half-inch hump. Again, much of the wealth ended up in Cave Creek, with various areas tabulating over 1.5 inches.

How To Get Rid of Mice — Easy Home Remedies as Inexpensive as They Are Effective: Pest Pro Reveals

Lindsey Bosslett – September 28, 2023

Ahh, we love the nip in the air that means fall is finally here. Unfortunately, the dip in outdoor temperatures means mice will be looking to take up residence in warmer surroundings, namely your home. If all through your house a creature is stirring, don’t worry — it’s easier than you think to banish mice. And it’s important to know: Not only are mice a nuisance, they can also import other pests, like ticks and mites, into your home. In fact, according to Discovery Wildlife, 42% of homeowners with an unwanted “mouse guest” will experience damage to their home’s structure and furnishings; 31% to food supplies; and 9% to insulation and wiring. And since a single mouse can give birth to 50 or more babies a year! We’ve tapped pest pros to give us the best way to get rid of mice without having to call…a pest pro!

How to tell if you have mice

Jose A. Bernat Bacete/Getty images

“Mice are primarily nocturnal, so the chances you’ll actually see one are low unless you’re a night owl,” explains Nicole Carpenter, pest control specialist with Black Pest. Signs you have one or more living among you include:

Holes chewed into boxes of food, pet food and litter

Holes chewed into furniture, blankets or pillows with stuffing disturbed

Cylindrical, pointy-ended droppings about 6 mm long

The smell of ammonia, which is caused by their urine

Hearing scurrying, squeaking or gnawing sounds in your walls, vents or ceiling

Seeing tooth marks in furniture, walls or wires

Dirty-looking smears along walls or floors, which is caused by the grease on their fur

Why mice can be hazardous to your health

Mice can carry several diseases that can be transferred to their human roommates, including hantavirus, leptospirosis, lymphocytic choriomeningitis, typhus and even the bubonic plague, according to the Centers for Disease Control. And though it’s rare to get sick from the rodents, it’s important to throw away any food they may have gotten into to ensure you stay disease-free.

How to get rid of mice: the best no-trap deterrent home remedies

If you’ve found signs that little critters have set up shop in your home, try the following simple home remedies to create a mouse-free zone without needing to trap and kill them:

1. The smell of peppermint

Jenny Dettrick/Getty Images

Mint is one of the best all-natural mice deterrents there is. “Mice really hate the smell and will go out of their way — even leave their cozy nests behind —to avoid it,” Carpenter reveals. “Just take some cotton balls, soak them in peppermint essential oil and leave them near spots you think the mice are active in your home.”

2. The smell of mothballs

Raunamaxtor/Getty

May as well call them miceballs, mothballs contain naphthalene and paradichlorobenzene — as these chemicals break down, they produce an odorous gas that creates that signature “mothball” scent. Mice not only find the smell unpleasant, the gas is also unhealthy for them, so they’ll take off for clearer air elsewhere. “Simply place mothballs near where you think the mice are nesting,” says Thomas.

3. The smell of white vinegar

Another scent mice won’t want to be around is white vinegar. Carpenter says there are two ways to put it to work: “First, you can soak cotton balls in white vinegar and put them where you suspect mice might be. Change these every few days to keep the vinegar smell strong. Or you can mix equal parts white vinegar and water in a spray bottle and spritz it along baseboards, corners and entry points. Repeat this as needed.”

How to get rid of mice: humane trap home remedies

Humane traps let you capture mice, then release them unharmed away from your home. Experts recommend driving at least two miles away, otherwise the mice will often try to return. A few to try: Wanqueen Humane Trap 4-pack, (Buy from Amazon, $12.99) or Harris Catch and Release Humane Mouse Trap 2-pack, (Buy from Home Depot, $14.39).

If you are considering using traps that kill mice, the best choice is a spring trap, which can be found at your local supermarket or dollar store and are the least likely to cause the mouse any suffering.

Most pest experts recommend staying away from glue traps due to cruelty, and from poisons, as these not only cause an unpleasant death for the mouse, but they can wind up perishing inside your walls or vents and be difficult to remove. Plus, if the bait or poisoned mouse is eaten by pets or other wildlife, they can wind up being poisoned, as well.

Can a cat help rid my home of mice?

Not all cats are interested in hunting, and even those who do like to stalk prey typically cannot tackle a true infestation. Bottom line: Kitties are great pets, but generally not a reliable form of mouse control.

How to keep mice from ever darkening your door

To avoid even needing to know how to get rid of mice using home remedies, the first line of defense is to keep mice out of your home in the first place, says Sean Thomas, owner of DIY pest control blog Conquer Critters. His easy how-tos:

1. Tweak your pantry

Food is one of the top reasons mice enter homes, according to Thomas, and they can detect scents up to 10 miles away — which means they can sniff out crumbs left on your counters and floors, as well as food left in paper or cardboard containers, which includes pantry staples like rice, cereal, oats, sugar and pasta. Give your kitchen a quick daily sweep to stay on top of crumbs, Thomas advises. “And store food in airtight, mouse-proof packaging.” Look for hard plastic food storage bins at the dollar store. Or you can buy entire sets, like the Mibote 28-piece airtight storage container set (Buy at Walmart, $49.99). Not only are they mouse-proof, they also keep your food fresher longer and can transform your pantry from cluttered to a beautifully curated space.

2. Plug sneaky leaks

LoveTheWind/Getty Images

Like every other creature, mice need water to live. “So if there are any leaking pipes or standing water, that can draw them in too,” Carpenter explains. Just do a quick check under sink cabinets and near drains in basements to make sure there are no water issues you need to address — in addition to mice, these can also cause mold and mildew problems that may impact your health. (Click through to learn more about how to get rid of mold in your bathroom.)

3. Bar common entry points

Shelter is the other top reason mice enter homes — most people believe they only invade in winter while looking for warmth, but they will also seek the cool, dry comfort of your house to escape the summer heat and rain.

“Shoring up your house from shelter-seeking mice takes a bit of a sharp eye,” says Thomas. “Mice have collapsible rib cages, which means they can flatten their bodies to fit in a tiny gap between, say, the bottom of your garage door and the floor, or a hole as small as 2 cm. They are also adept climbers, so the entryways don’t need to be ground-level.”

Where to check for mice

When looking for mouse entryways, grab a flashlight and check these areas key inside your home:

Around doors and windows

Inside cabinets, particularly the kitchen and bathrooms

Along baseboards and near vent openings

Behind appliances

Around pipes and floor drains

Along basement walls and crawl spaces

Then head outside and inspect these spots:

The foundation

Around pipes, gas lines or electrical wiring

The garage door and walls

Around any weather stripping

Any outdoor vents and airways

Attic windows

See holes and gaps? A home remedy that works: Use copper or steel wool to fill in holes, as mice typically won’t put in the effort to chew through it.

Or, you can fill them in using expandable mouse-proof foam insultation, such as DAP Mouse Foam Sealant, (Buy from Amazon, $18.62) or Smart Dispenser 12 oz. Pestblock Insulating Spray Foam Sealant, (Buy from Home Depot, $9.97)

These Are the Best Mouse Traps, Whether You Prefer to Snap, Zap, or Catch and Release Them

Kevin Cortez, Alex Rennie – September 27, 2023

The Best Mouse Traps for Getting Rid of RodentsVictor

“Hearst Magazines and Yahoo may earn commission or revenue on some items through these links.”

Whether you think mice are pests to be eliminated by any means necessary or simply cute and cuddly guests to be relocated, one thing is true: They need to be removed. And you should know how to get rid of mice. Although serious infestations will require a professional pest control expert, there’s still a lot you can do to mitigate your rodent problem by employing mouse traps. These are designed to be easy to use, and since they’re available in a variety of types and sizes, you can choose exactly how you’d like to deal with captured mice.

Catch and Release (No-Kill), Snap Traps (Kill), or Glue (Either/Or)

The most important thing to remember when choosing a mouse trap is whether or not you want to kill your mice or keep them alive after they’re caught. If you’d prefer not to kill the unwanted houseguests, choose a “catch and release” trap. These contraptions usually feature a mechanism that allows the mouse to enter then quarantines them inside until you can transport them to wherever you plan to release them. They’re also typically reusable and come in various sizes, from catching one mouse to up to 10. Catch and release is considered, naturally, a humane pest control tactic. When releasing, just be careful not to make contact with any urine or droppings to prevent exposure to hantaviruses.

Choose a snap-style or glue trap if you plan to kill your mice. Snapping traps do just that: snap their jaws onto the mouse once the animal steps on the trigger. These are usually disposable as, once a mouse has been killed in it, other mice will tend to avoid it.

Glue traps are another lethal option and use a strong adhesive to trap and immobilize the mouse when it steps on it, eventually killing it. Although we have been able to use glue traps without killing the mice they caught (we used olive oil to free them successfully), you should consider these traps lethal. Rats often get stuck and will rip off their skin and fur when trying to escape them, so be mindful of this if you consider the glue trap. All glue traps are made with nontoxic adhesive, so if a small child or pet accidentally touches one, they won’t be exposed to harmful chemicals or poisons. However, the CDC does not recommend glue traps as they can scare mice and rats, causing them to urinate, which can increase risk of rodent-related illnesses.

We don’t recommend using poisons. These baits and pellets cause rats and mice to die slowly over time, resulting in dead bodies scattered around the house—maybe inside your walls or in other hard-to-reach areas. That can also create an odor that’s difficult to locate and, therefore, clean up. Poisons also cause rodent bodies to become poisonous, thus poisoning any animal that may eat a carcass—pets included.

Bait

Regardless of what kind of trap you choose, you’ll need bait. Some traps include gel baits that attract mice to their scent, while others require you to use something that you may already have to invite mice, like food. Pest control companies often recommend loading traps with small bits of cheese, nut butter, chocolate, or seeds. Be careful not to overload a trap, as mice may easily be able to grab pieces without setting them off. Too much bait also risks attracting other pests like roaches and ants.

How We Selected

We’ve used nearly every mouse trap and took that experience, as well as several hours of research, to determine which are the best. We considered advice, guides, and explainers from various pest control services and publications to find what makes a mouse trap effective, and, importantly, only chose lures with nontoxic additives. No poisonous baits were considered, as they’re too dangerous for homes with animals and children. We did our best to include a range of trap sizes, so whether you’re in a studio apartment with minimal room or need help controlling an outdoor infestation, you’ll find a trap that best suits your living space. Because there isn’t much variation among traps of a certain type between brands, we selected only six as the best: two catch-and-release, two snap, and and one glue trap, plus an electric option for the quickest kill possible.

Press ’N Set Mouse Trap

This snap trap served us well during a particularly aggressive mouse infestation. It’s extremely simple to set up, so there’s minimal risk of pinched fingers. You just press the rear tab, the jaw opens, and the trap is ready to go.

Best of all, the top jaw has a handy cutout, so you can bait the trigger before you even expose the teeth. Despite this simple operation, the trap is stronger than you might think, and ours was even able to catch three mice in a single snap. Its white plastic body is also easier on the eyes than black or metal traps, which was a nice perk.

Shop NowPress ’N Set Mouse Trapamazon.com$36.86More

M154 Mouse Trap

If you’re looking to trap several mice but don’t have the budget for more expensive disposable traps, this classic Victor snap trap is a great fit—given you’re okay with kill traps. You get a dozen with each purchase, making it ideal for placing along a runway or area that rodents frequently use, increasing chances of success.

This old-school, prototypical mouse trap isn’t as easy to set as newer traps—it has more tension when setting them. Relatedly, users find the trigger less sensitive than on other traps, and featherweight or younger mice may not be heavy enough to set it off. Others say it’s fragile and, while labeled reusable, is likely not. Still, most users say this classic trap is the way to go, as it instantly kills mice, thus, limiting exposure to potential rodent-related diseases via droppings or urine—no wait, and minor cleanup.

This lethal trap features a unique system to destroy the mice it captures—using an electric current to quickly electrocute any rodents that walk inside its “kill chamber.”

The chamber is detachable, so it’s easy to empty and clean out and allows you to re-bait it before reattaching. A green indicator light also lets you know as soon as a mouse is caught and will stay lit for up to a week so that you won’t miss it.

Replacing batteries in any tool can be inconvenient, but since this model can kill 100 mice per charge, you won’t need to switch them out often.

Shop NowM250S No Touch, No See Mouse Trapamazon.com$78.23More

Heavy Duty Glue Mouse Trap

This Catchmaster glue trap covers a large surface area—10 by 5 inches—which increases your chances of trapping your furry intruders. They’re simple to use—just pull the two boards apart and place them on the ground—and should last for up to a year under normal circumstances.

Plus, the integrated floor anchors (tabs of putty at each corner of the trap) keep them in place, even if your mouse tries to pull them away. The large size of these traps might not make them the most practical choice for heavy traffic areas like your kitchen, where pets or kids might accidentally get stuck.

This RinneTrap bucket trap is designed to humanely capture multiple mice, making it well-suited for barns, warehouses, or anywhere else with large mice populations that need removing.

A simple ramp and tipping lid means no poisons or chemicals on your property. You simply attach this device to a standard 5- or 20-gallon bucket, load it with bait, check the trap, and release the rodents if full. It doesn’t include the required bucket, though you should be able to find one at your local hardware store. RinneTraps are quite pricey when compared to other traps here, however.

Shop NowFlip N Slide Mouse Trapamazon.com$34.99More

M310SSR Tin Cat Multi-Catch Live Mouse Trap

The Victor Tin Cat mouse trap is large enough to catch up to 30 mice before reaching capacity, but its 1.9-inch height still makes it compact enough to use in your home without taking up too much space. Its cutout window lets you know when a mouse is inside, and the lid is simple to open, so you can quickly release them whenever ready.

Its metal construction ensures a mouse can’t simply open its list and slip out, plus it makes cleaning bait, like peanut butter and cheeses, off its surface. This trap is safe for kids and animals and can be reused or disposed of when finished.

Some users say it’s ineffective for catching small and baby mice, as they can slip through the trap’s openings. Others note that it works well when used outdoors and can withstand mild weather like rain and snow.

Shop NowM310SSR Tin Cat Multi-Catch Live Mouse Trapamazon.com

Judge Rules That Donald Trump Committed Fraud While Building Real Estate Empire

Virginia Chamlee – September 27, 2023

The ruling allows a civil trial against Trump and his adult sons to move forward next week, and orders that some of the former president’s companies be dissolved

James Devaney/GC Images Donald Trump leaves Trump Tower in Manhattan on March 9, 2021

A New York judge ruled on Tuesday that Donald Trump lied on financial statements about the value of the properties in his real estate portfolio and was therefore able to secure favorable loan terms and lower insurance premiums.

In a 35-page ruling, Judge Arthur Engoron said that Trump and his organization had overvalued several of it’s properties, including the members-only Mar-a-Lago club in Palm Beach, Florida.

In court filings, Trump has pegged the property’s worth at between $426.5 million and $612.1 million. But Engoron cited a Palm Beach County assessor who appraised Mar-a-Lago’s market value to be between $18 million and $27.6 million — at least 2,300 percent less than what the former president has claimed.

In the ruling, the judge adds that some of the former president’s defenses — such as arguing that square footage is “subjective” — are “absurd.” The ruling further sanctions Trump’s attorneys $7,500 each for continuing to make legal arguments that had already been rejected in court twice, and requires that some LLCs associated with Trump be dissolved.

Tuesday’s ruling allows a civil trial into the outstanding claims (to be decided by the judge, with no jury) to begin next week.

The ruling came as part of a fraud case brought against the former president, his adult sons Eric Trump and Donald Trump Jr., and their company the Trump Organization, by New York State Attorney General Letitia James.

“Today, a judge ruled in our favor and found that Donald Trump and the Trump Organization engaged in years of financial fraud,” James said in a statement. “We look forward to presenting the rest of our case at trial.”

James has accused the Trumps and their company of fraudulently inflating the former president’s fortune by as much as $2.2 billion since 2011. The lawsuit aims to have Trump banned from doing business in New York and pay $250 million.

Engoron’s ruling alleges that the inflation of Mar-a-Lago’s worth is akin to fraud. From the ruling: “A discrepancy of this order of magnitude, by a real estate developer sizing up his own living space of decades, can only be considered fraud.”

Joe Raedle/Getty Donald Trump’s Mar-a-Lago resort in Palm Beach, Florida

An earlier court filing alleges that “correcting for these and other blatant and obvious deceptive practices engaged in by Defendants reduces Mr. Trump’s net worth by between 17-39% in each year, or between $812 million to $2.2 billion, depending on the year.”

The filing accused Trump of valuing several of his properties “at amounts that significantly exceeded professional appraisals of which his employees were aware and chose to ignore.” In one alleged instance, he valued his leased property on Wall Street at more than twice the amount of the appraised value.

Trump and his sons have both fired back at the recent ruling regarding the worth of Mar-a-Lago, with Eric claiming on Twitter: “Mar-a-Lago is speculated to be worth we’ll [sic] over a billion dollars.”

Trump himself also disputed the ruling, writing an angry missive on his social media site Truth Social in which he accused the judge of being “a Deranged, Trump Hating Judge, who RAILROADED this FAKE CASE through a NYS Court at a speed never seen before, refusing to let it go to the Commercial Division, where it belongs, denying me everything, No Trial, No Jury.”

Trump added that Mar-a-Lago is “WORTH POSSIBLY 100 TIMES” what Engoron cited in his ruling, adding: “My actual Net Worth is MUCH GREATER than the number shown on the Financial Statements, a BIG SURPRISE to him & the Racist A.G., Letitia James, who campaigned for office on a get Trump Platform.”

Since leaving office in January 2021, Trump’s post-White House prestige has been overshadowed by intensifying investigations on various fronts, including into his political conduct and business affairs.

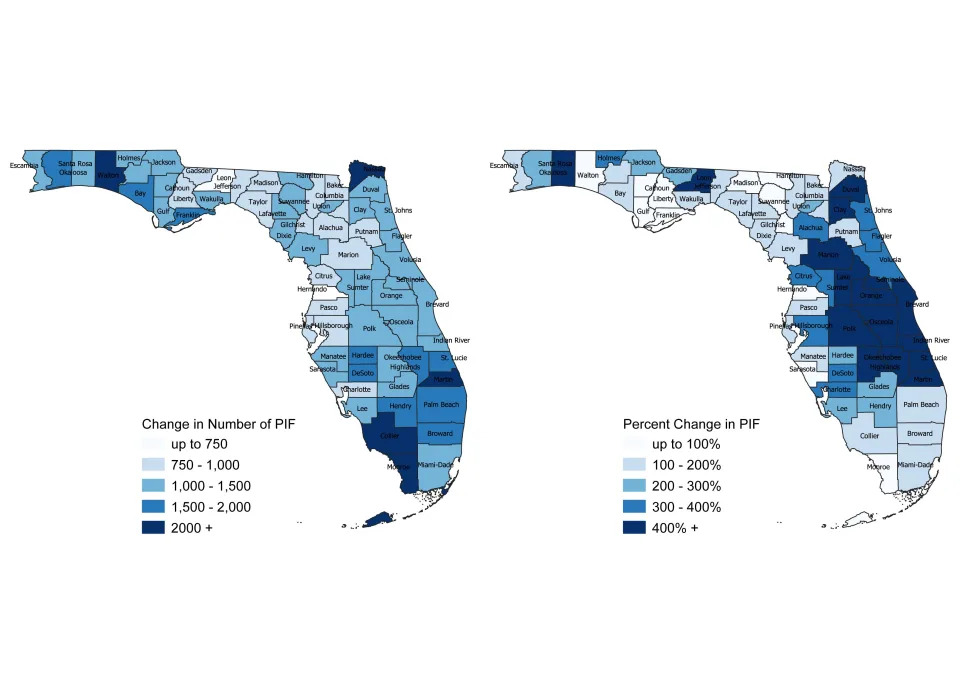

Florida’s coastal homes may lose value as climate-fueled storms intensify insurance risk

Kate Cimini, USA TODAY- Florida – September 25, 2023

Climate-fueled disasters like Hurricane Ian are wreaking havoc on home values across the nation, but Florida’s messy insurance market makes it one of the most stressed, new research out of a nonprofit climate modeling group indicates.

High insurance premiums and a state-backed requirement that homeowners covered by the state-backed insurer of last resort enroll in the National Flood Insurance Program over the next three years could drop home values up to 40% in Florida in the next 30 years, data provided by First Street Foundation shows. And climate and insurance experts say that may further gentrify Florida’s coastal regions and barrier islands.

Using what First Street representatives described as a typical institutional-investing calculation, First Street Foundation found some homes, adjusting for 2023 insurance costs, have already lost up to 19% of their value.

The News-Press reported earlier this month on middle-class families being forced off Fort Myers Beach due to the rising costs associated with living on a barrier island in a time of stronger storms, including more stringent, expensive building requirements and a high demand for Beach property.

Experts say this trend will likely continue in coastal communities as high-income buyers who can afford to go without insurance rebuild and repair out of pocket. They say it will take a concerted effort among state and federal officials, as well as insurance and reinsurance companies to avoid climate-spurred migration and subsequent gentrification of Florida’s coast.

Do property values go down after a hurricane in Florida?

Geographer Zac Taylor, a professor with the Delft University of Technology in Norway, studies the connection between climate change and the insurance industry in Florida. Taylor uses they/them pronouns.

They urged caution in reassessing home values but agreed that this was a possible outcome based on current climate models.

Some of Florida’s more vulnerable coastline may even see corporations purchasing homes with the intent to rent them out, Taylor said, though real estate investor purchases of single-family homes dropped 45% in the second quarter of 2023, compared to a year ago, per realty company Redfin.

Soon, “only wealthy people will be able to afford to remain in coastal areas,” said Taylor.

What areas are being gentrified in Florida?

Gentrification of Florida’s coastline may have already begun in areas hardest-hit by Ian.

This is likely to continue as a number of factors drive up the costs associated with living along the Sunshine State’s coast thanks to sea level rise, a 2022 study out of Florida State University predicted.

“Eventually, people are likely to start moving inland from coastal areas as the costs of staying become too great,” the report reads. “Those that are further inland are more likely to be displaced by higher income residents who eventually move inland in the process of relocating to higher ground.”

On Pine Island, a community whose year-round residents are largely working-class, people are cutting back their monthly budgets and searching desperately for cheaper insurance after rates rose in response to Hurricane Ian’s devastation of the barrier island. Some are leaving the island after too many problems with insurance, said nonprofit civic group Matlacha Hookers president Joanne Correia.

Guylinda DeMyers and her husband have lived in Pine Island’s St. James City for 20 years, she estimates, but after this most recent hurricane, she said they plan to sell their home and leave for safer climes − once their insurance company pays their claim.

They’ve yet to see a penny of their claim from People’s Trust, she said, even though it’s been almost a year. In fact, it’s been so long, their policy has expired. They haven’t pursued a new one because “there’s nothing to insure,” DeMeyers said. “It’s broken.”

She doesn’t think they’ll get what the home was worth before the storm, but says her realtor has told her the property itself – an ocean-front lot ‒ is valuable enough by itself.

But DeMeyers is determined to see her claim through – if not for her, then for her husband, who has Alzheimer’s. She’s lived through three major hurricanes and subsequent rising insurance costs.

“It’s not safe here anymore,” DeMeyers said. “We need a stable place.”

On Fort Myers Beach, another one of Florida’s vulnerable barrier islands, coastal gentrification is already underway. Renters and low-income homeowners are finding there’s nothing in their budget on the island anymore. The island is home to just 5,700 residents year-round, and the loss of even a few is significant.

“I feel like I’ve lost my community,” former Fort Myers Beach resident Cheri Warren told Chad Gillis of The News-Press in early September. Warren’s one-story home was destroyed during Hurricane Ian; now, she and her husband found it was too costly to repair it and have left the barrier island for the mainland. They plan to sell their lot at a later date, when the market has stabilized.

Has home insurance gone up in Florida?

For its new study, released in September, First Street Foundation founder and CEO Matthew Eby said the nonprofit, like institutional investors, calculated home values by dividing the amount of what a property would rent for over the course of a year, minus operating costs (which includes insurance costs), by 5%, an average risk amount.

While most homeowners look at the prices their neighbors homes are selling for in order to figure out how much theirs could be worth, this approach can take a while to show fluctuations in real home value, said First Street Foundation’s head of climate implications Jeremy Porter. Institutional investors use a standard calculation that First Street Foundation employed to “take the uncertainty out of the equation,” he said.

But with the cost of insurance rising due to both inflation and natural disasters like hurricanes and fires, risks increase as well. That means that operating costs have increased, particularly for Floridians who have no option for insurance other than state-created nonprofit Citizens Property Insurance Corporation. Citizens was created to insure homes that all other carriers refused to insure − the riskiest properties.

Not only is Citizens often more expensive than other carriers, as state law allows them to charge an actuarially-sound amount, but Florida legislators recently passed a law requiring homeowners who get their insurance through Citizens also enroll their homes in the National Flood Insurance Program, a federal insurance program.

That increases a homeowner’s operating costs even further.

“When … you don’t have anywhere else to go and you are beholden to whatever increase in prices that they just decide to put on you, there’s no way out,” Eby said.

Since 2017, Citizens’ number of policies have increased 168%, while the average premium has also increased from roughly $2,000 to more than $3,000 annually.

Citizens spokesman Michael Peltier said Citizens is held to a policy premium increase of 12% annually, and increases are subject to state approval.

Although California and Louisiana are facing rocketing insurance costs as well, according to First Street Foundation’s data, Eby said, “Florida has the biggest problem.”

The nonprofit examined the number of policies Citizens holds in Florida going back to 2017, when Citizens held roughly 500,000 policies. Eby noted that increased over time, and dramatically grew in 2021 as private insurance companies began to pull out of the state. After Ian, it shot up once again.

Citizens currently holds 1.5 million policies in force, and, Peltier said, expects that to increase to 1.7 million by the end of 2023.

“The major insurance companies have all been pulling out of Florida, leaving Citizens the largest insurer in the state,” said Eby. “The insurance company of last resort, the very last one that you want to go to for your insurance, is now the insurer for the entire state.”

Rising homeowners’ insurance bill have yet to translate that to loss of equity, Porter said.

“When you go to sell it, that’s when the property devaluation becomes realized – at the closing table,” Porter said. But even those who hang on to their homes may feel it the next time Florida gets hit by another major weather event like Ian, he cautioned.

Then, he said, taxpayers will be the ones hurting.

“At some point, the amount of exposure on Citizens is too much, relative to its premiums,” said Porter. “If it’s not accounted for properly there has to be some kind of a subsidy from Florida taxpayers one way or another.”

Eventually, Porter predicted, “the state of Florida is going to have to ask the federal government for a bailout if they if they end up getting hit by a disaster that empties the coffers.”

According to Peltier, Citizens has a number of backstops to keep itself solvent. First, he said, if the state-created nonprofit goes through its premium-driven surplus, like all other insurers in the state it has access to the Florida hurricane catastrophe fund. It also purchases reinsurance to cover the possibility that the catastrophe fund is exhausted. Finally, Peltier said, Citizens is required by law to levy assessments on policyholders to make up any deficits.