Study: Cancer-causing gas leaking from CA stoves, pipes

Drew Costley – October 20, 2022

Gas stoves in California homes are leaking cancer-causing benzene, researchers found in a new study published on Thursday, though they say more research is needed to understand how many homes have leaks.

In the study, published in Environmental Science and Technology on Thursday, researchers also estimated that over 4 tons of benzene per year are being leaked into the atmosphere from outdoor pipes that deliver the gas to buildings around California — the equivalent to the benzene emissions from nearly 60,000 vehicles. And those emissions are unaccounted for by the state.

The researchers collected samples of gas from 159 homes in different regions of California and measured to see what types of gases were being emitted into homes when stoves were off. They found that all of the samples they tested had hazardous air pollutants, like benzene, toluene, ethylbenzene and xylene (BTEX), all of which can have adverse health effects in humans with chronic exposure or acute exposure in larger amounts.

Of most concern to the researchers was benzene, a known carcinogen that can lead to leukemia and other cancers and blood disorders, according to the National Cancer Institute.

The finding could have major implications for indoor and outdoor air quality in California, which has the second highest level of residential natural gas use in the United States.

“What our science shows is that people in California are exposed to potentially hazardous levels of benzene from the gas that is piped into their homes,” said Drew Michanowicz, a study co-author and senior scientist at PSE Healthy Energy, an energy research and policy institute. “We hope that policymakers will consider this data when they are making policy to ensure current and future policies are health-protective in light of this new research.” 0:01 0:38 Scroll back up to restore default view.

Homes in the Greater Los Angeles, the North San Fernando Valley, and the San Clarita Valley areas had the highest benzene in gas levels. Leaks from stoves in these regions could emit enough benzene to significantly exceed the limit determined to be safe by the California Office of Environmental Health Hazards Assessment.

This finding in particular didn’t surprise residents and health care workers in the region who spoke to The Associated Press about the study. That’s because many of them experienced the largest-known natural gas leak in the nation in Aliso Canyon in 2015.

Back then, 100,000 tons of methane and other gases, including benzene, leaked from a failed well operated by Southern California Gas Co. It took nearly four months to get the leak under control and resulted in headaches, nausea and nose bleeds.

Dr. Jeffrey Nordella was a physician at an urgent care in the region during this time and remembers being puzzled by the variety of symptoms patients were experiencing. “I didn’t have much to offer them,” except to help them try to detox from the exposures, he said.

That was an acute exposure of a large amount of benzene, which is different from chronic exposure to smaller amounts, but “remember what the World Health Organization said: there’s no safe level of benzene,” he said.

Kyoko Hibino was one of the residents exposed to toxic air pollution as a result of the Aliso Canyon gas leak. After the leak, she started having a persistent cough and nosebleeds and eventually was diagnosed with breast cancer, which has also been linked to benzene exposure. Her cats also started having nosebleeds and one recently passed away from leukemia.

“I’d say let’s take this study really seriously and understand how bad (benzene exposure) is,” she said.

Trump drops F-bombs and shares potentially sensitive information in newly released audio

Stephen Proctor – October 19, 2022

Previously unheard audio featuring former President Donald Trump aired Tuesday on Anderson Cooper 360. Famed journalist Bob Woodward recorded 20 conversations he had with the former president, with Trump’s knowledge, from 2016 through 2020. Trump, who is facing possible legal peril for taking classified documents when he left office, appears in one recording to share sensitive information with Woodward.

“I have built a weapons system that nobody’s ever had in this country before,” Trump said. “We have stuff that you haven’t even seen or heard about. We have stuff that Putin and Xi have never heard about before.”

Trump also spoke of Russia’s nuclear capabilities.

“Getting along with Russia is a good thing, not a bad thing, alright?” Trump said. “Especially because they have 1,332 nuclear f***ing warheads.”

Throughout his presidency, Trump was criticized for his apparent affinity for authoritarian leaders, which he spoke about to Woodward.

“It’s funny, the relationships I have, the tougher and meaner they are, the better I get along with them. You know? Explain that to me someday, OK,” Trump said. “But maybe it’s not a bad thing. The easy ones are the ones I maybe don’t like as much or don’t get along with as much.”

In another recording, Trump brags about how he handled being impeached, while at the same time taking shots at two of his predecessors who also faced impeachment.

“There’s nobody that’s tougher than me,” Trump said. “Nobody’s tougher than me. You asked me about impeachment. I’m under impeachment, and you said, you know, you just act like you won the f***ing race. Nixon was in a corner with his thumb in his mouth. Bill Clinton took it very, very hard. I just do things, OK?”

In 2016, Woodward asked then-candidate Trump about having his staff sign non-disclosure agreements. Woodward recorded Trump talking to his staff about who had and who had not yet signed one. Trump was confident in the effectiveness of these agreements at the time, but a multitude of former officials wrote tell-all books after leaving the administration.

Woodward plans to release the more than eight hours of recordings as an audiobook titled The Trump Tapes on Oct. 25.

The real story behind America’s population bomb: Adults want their independence

Clay Routledge and Will Johnson – October 12, 2022

Declining birth rates are a major concern for the United States and many countries around the world, so we – an expert in existential psychology and an expert in pulsing public opinion – surveyed the Americans choosing not to have children to learn the reasons why.

Americans are having fewer children than are needed to keep population numbers stable.

Fear of not just climate change and affordable housing

Much of the conversation in the United States about this issue has focused on fears about the future of the world or major economic challenges. For instance, the threat of climate change and the affordability of housing are frequently referenced as reasons that Americans don’t want to have kids.

While those are concerns of course, when you look at the data, family planning appears to be influenced more by people’s personal views about the independent life they want to live than their worries about potential environmental or economic issues.

This has important implications for how we as a nation approach the demographic challenge of declining birth rates.

A Harris Poll found that of those without children, about half do not want to have a child in the future, while 20% remain unsure. The only factor that the majority (54%) of Americans who don’t want to have kids endorsed as influencing their decision was maintaining personal independence.

We then asked these individuals whether their decision to not have children was influenced by a wide range of factors. Only 28% of them reported that climate change influenced their decision to not have kids. Similarly, only 33% indicated that housing prices influenced their decision.

Other factors we asked about including the political situation in the United States (31%), safety concerns (31%), personal financial situation (46%) and work-life balance (40%) were endorsed by less than half of respondents.

The only factor that the majority (54%) of Americans who don’t want to have kids endorsed as influencing their decision was maintaining personal independence.

Moreover, since respondents were able to indicate multiple reasons for not having kids, we also asked them which of those factors most influenced their decision. Further suggesting that this decision is more about personal preferences than other factors, we found that maintaining personal independence was reported as the most influential factor for more respondents than any other factor; 43% of those who considered independence to be a factor indicated that it was the most influential reason for not having kids.

For comparison, only 26% of those who considered climate change when deciding whether to have children reported that it was the most influential reason and only 9% of those who considered housing prices indicated such.

Americans may have multiple reasons for opting out of parenting, but their desire for personal independence is the most powerful one.

It is also worth noting that men and women were generally similar in their reasoning; 53% of females and 55% of males reported that their desire to maintain their personal independence influenced their decision to not have children. No other reason for not having kids was cited by a majority of men or women.

We shouldn’t oversimplify the story of why more and more Americans are choosing to not start families. It is undoubtedly complex and involves facets that public opinion surveys can’t fully capture. However, our results have important implications for cultural and political discussions around this issue.

Changes in public policy may not help

Perhaps most important, our findings suggest that public policy solutions are unlikely to have much impact on birth rates. Because Americans who are opting out of having children are more influenced by their desire to maintain their personal independence than concerns about climate change or affordable housing, or other issues such as work-life balance and safety, efforts to promote a more pro-natal society will need to be more cultural in nature.

More specifically, these efforts will need to address psychological needs related to individuals’ life goals and priorities.

How do we change people’s attitude about how children will affect their lives if they privilege personal freedom over other ideals? A good place to start is to focus on one of the most fundamental psychological needs, the need for existential meaning.

Humans are highly motivated to perceive their lives as meaningful. And it is when they perceive their lives as full of meaning that they are most mentally healthy, resilient, goal-driven, self-disciplined and self-reliant. In this way, meaning can be thought of as a key ingredient to achieving personal independence.

The Americans concerned about how having children may affect their personal independence may not realize that meaning is so empowering and that family is a fundamental source of meaning. For instance, surveys find that when people are asked what makes their lives feel meaningful, the most common response is family.

In addition, studies find that parents report higher levels of meaning than adults without children and have a greater sense of meaning when they are taking care of their children than when they are engaged in other activities.

Cultural narratives that treat parenting as a threat to personal independence and a roadblock to a fulfilling life may contribute to declining birth rates more than many realize.

There are of course environmental, economic and other challenges that can make people worried about bringing another human into this world and that can make raising children difficult.

But this is not new. For much of our history, most humans lived far more perilous lives than we live today. Our challenge is less about our material conditions and more about our mindset.

If we want a world with more children, we are going to have to convince people that having and raising kids is a critical ingredient of, not a barrier to, the good life.

Republicans Plan to Use Debt Limit Leverage to Reduce Social Security, Medicare: Report

Michael Rainey – October 12, 2022

Republicans in the House are planning to use a potential showdown next year over raising the federal debt limit to make changes in Social Security and Medicare, Bloomberg’s Jack Fitzpatrick reports.

The developing plan hinges on Republicans winning control of the House in the midterm elections, an outcome that is looking likely. Four GOP lawmakers who are vying for leadership of the House Budget Committee in the event of a Republican victory told Fitzpatrick that the need to raise the debt ceiling could give them the leverage they need to force Democrats to make concessions.

“The debt limit is clearly one of those tools that Republicans — that a Republican-controlled Congress — will use to make sure that we do everything we can to make this economy strong,” Rep. Jason Smith (R-MO), the senior Republican on the current Budget Committee, said.

Republicans are still discussing exactly what changes they might try to enact. “What would we consider a win?” said Rep. Lloyd Smucker (R-PA), who is interested in the top spot on the Budget Committee. “What would we consider to be a fiscally responsible budget?”

Although the details are still up in the air, one theme is clear: House Republicans want to reduce federal spending, and the major entitlement programs are a target. Rep. Buddy Carter (R-GA) Carter said that Republicans’ “main focus has got to be on nondiscretionary — it’s got to be on entitlements.”

Shrinking the safety net: One option reportedly being discussed is raising the eligibility age for Social Security and Medicare, the two largest mandatory spending programs. Each faces financial squeezes in the coming years as the baby boomers age and continue to retire. Under current rules, the Social Security system would be forced to cut benefits starting in 2034, while Medicare could run short of funds by 2028.

Earlier this year, the Republican Study Committee released a plan to raise the eligibility age for Social Security to 70 and the eligibility age for Medicare to 67. The increases would be phased in over time and once the target is reached, the eligibility age would then be indexed to life expectancy. The lawmakers also called for increased means testing in the Medicare program, and a privatization option for Social Security.

Other options being considered include more stringent work requirements and income limits for what Smith called “welfare programs,” including the Supplemental Nutrition Assistance Program more commonly known as food stamps. And new caps on discretionary spending could limit spending increases over 10 years.

One thing that won’t be cut: defense spending. Rep. Jodey Arrington (R-TX) told Bloomberg that he wants to cut nondefense spending in order to provide more money for the military.

Willing to risk “catastrophe”? Republicans say they are leery about pushing too far in their demands, but many experts think that any effort to use the debt limit as leverage in negotiations is unacceptably risky. Treasury Secretary Janet Yellen has warned that defaulting on U.S. debt payments — which would occur if the U.S. failed to raise the debt ceiling — would cause a “catastrophe” in the global economy.

Speaker Nancy Pelosi (D-CA) accused the GOP of taking huge risks in order to cut important social programs. “House Republicans are openly threatening to cause an economic catastrophe in order to realize their obsession with slashing Medicare and Social Security,” a Pelosi spokesperson told Bloomberg. “As House Republican leaders’ own words constantly reveal, dismantling the pillars of American seniors’ financial security is not a fringe view in the extreme MAGA House GOP, it is a broadly held obsession at the core of their legislative agenda.”

House Budget Committee Chair John Yarmuth (D-KY) also criticized Republican plans. “Holding the full faith and credit of the United States hostage to implement an extreme and unpopular agenda is not governing, it’s desperation,” Yarmuth said in a statement. “Congressional Republicans are so hellbent on gutting Social Security and ending Medicare as we know it that they are willing to risk economic catastrophe to get it done. This is a desperate attempt to shower the wealthy and big corporations with even more tax giveaways by intentionally sacrificing the needs of American families.”

Democrats do have one option for disarming Republicans ahead of a debt ceiling showdown: They could attempt to raise the ceiling on their own during the lame-duck session at the end of the year, potentially denying the GOP the use of that weapon. But both Yarmuth and Sen. Tim Kaine (D-VA) told Bloomberg there has been no discussion among Democrats about such a plan.

The bottom line: Taking a page from the tea party playbook from a decade ago, expect to see Republicans attempting to force spending reductions in the next Congress — reductions that could involve fundamental changes in the way the country’s top safety net programs operate.

Spanish Vineyards Use Solar Panels to Protect Wine Grapes

By Paige Bennett, Edited by Irma Omerhodzic – October 12, 2022

As global wineries are hit with impacts of climate change, a new project called Winesolar in Spain is innovating ways for vineyards to protect their grapes while also generating clean energy.

Iberdrola, an energy company based in Bilbao, Spain, has created a shelter for growing wine grapes at vineyards in Guadamur. The shelter is made with a few solar panels that generate about 40 kW of energy, which will be used by the González Byass and Grupo Emperador wineries. The solar panel shelter creates a microclimate by shading or exposing plants from the sun and offering some relief from high temperatures while also minimizing evaporation after watering crops.

While combining solar energy and agricultural land is not new, one component that makes the Winesolar project stand out is that it will have a tracking system, with trackers from PVH, that uses artificial intelligence (AI) to determine the most efficient solar panel positioning over the vines at any time, according to Iberdrola. Techedge, an IT firm, will help the solar panel project further the wineries’ agricultural goals.

Sensors in the vineyards will record data including soil humidity, wind conditions, solar radiation, and even vine thickness to find the optimal position for the solar panels, giving the vines a fighting chance against the effects of climate change.

“The installation will help to improve the quality of the grapes, allow a more efficient use of the land, reduce the consumption of irrigation water and improve the crop’s resistance to climatic conditions in the face of rising temperatures and increasingly frequent heat waves,” Iberdrola explained in a statement.

While the project is a small pilot, Iberdrola has plans to expand the idea into other Spanish vineyards, in addition to adding another 1,500 megawatts of solar panels across Spain. The company has installed 2,200 MW so far in 2022 and installed 800 MW last year, as CleanTechnica reported.

The project is an example of growing interest in agrovoltaics, or a balance between photovoltaic energy and agriculture through the installation of solar panels on farms. Agrovoltaic projects are meant to improve sustainability and make farming more efficient. While it isn’t a new concept — it was first conceived in the early 1980s — it has become increasingly popular in recent years for its potential environmental and economical benefits.

“When it comes to the environment, the main benefit of agrovoltaics is that it reduces greenhouse gas emissions from the agricultural sector,” Iberdrola said on its website. “What’s more, the dual use of land for both agriculture and for energy relieves pressure on ecosystems and biodiversity, which are affected when cultivation areas are expanded.”

Climate change is causing more billion-dollar weather disasters

David Knowles, Senior Editor – October 12, 2022

When Hurricane Ian barreled into Florida’s Gulf Coast last month, it became the 15th extreme weather event in the U.S. this year to rack up damages totaling more than $1 billion. Climate change, data shows, is helping to make expensive disasters much more frequent in recent years.

“In the last five years [2017-2021], there were just 18 days on average between billion-dollar disasters—compared to 82 days in the 1980s,” Climate Central, a consortium of scientists and journalists, found in a new analysis posted to its website.

This year’s extreme weather disasters in the U.S. have resulted in over 340 deaths, the NOAA said, and the financial toll is still being tallied. The insurance losses alone from Hurricane Ian are projected to cost between $53 billion and $74 billion, according to an estimate by RMS, a risk modeling company. In addition to that staggering sum, the National Flood Insurance Program could face an extra $10 billion in losses, Insurance Business America reported.

“The number and cost of weather and climate disasters are increasing in the United States due to a combination of increased exposure (i.e., more assets at risk), vulnerability (i.e., how much damage a hazard of given intensity — wind speed or flood depth, for example — causes at a location), and climate change is also supercharging the increasing frequency and intensity of certain types of extreme weather that lead to billion-dollar disasters — most notably the rise in vulnerability to drought, lengthening wildfire seasons in the western states, and the potential for extremely heavy rainfall becoming more common in the eastern states,” Adam Smith, a climatologist at the National Centers for Environmental Information and a lead analyst on the NOAA’s findings on $1 billion disasters, told Yahoo news in an email. “Sea level rise is worsening hurricane storm surge flooding.”

While climate change is not the sole cause of events like hurricanes, drought, rainfall or wildfires, ample scientific research has shown that rising global temperatures are amplifying all of them, making each potentially more destructive.

Workers clearing debris in Fort Myers, Fla., in the wake of Hurricane Ian, Oct. 1. (Giorgio Viera/AFP)

“The year-to-date average temperature for the contiguous U.S. was 56.8 degrees F — 1.7 degrees above average — ranking in the warmest third of the YTD record. California and Florida saw their third- and fourth-warmest January-through-September periods on record, respectively,” the NOAA stated on its website.

Across the West, nearly 1,000 heat records were broken in early September, the NOAA said, a month that will go down as the fifth-warmest on record. In all, the last seven years have been the warmest on record, according to data from NASA, the NOAA and Berkeley Earth.

The Intergovernmental Panel on Climate Change has for years been sounding the alarm about the risks related to global temperature rise and tried to convince world governments to agree to limit greenhouse gas emissions so as to keep average temperatures from rising above 1.5 degrees Celsius (2.7 degrees Fahrenheit) above preindustrial levels.

In its most recent report, which was issued in February, the IPCC reiterated that the planet could expect an increase in the kinds of severe weather consequences seen in recent years that have been liked to climate change.

“This report is a dire warning about the consequences of inaction,” Hoesung Lee, chair of the IPCC, said in a statement that accompanied the release of the report. “It shows that climate change is a grave and mounting threat to our well-being and a healthy planet. Our actions today will shape how people adapt and nature responds to increasing climate risks.”

Hurricane risk might seem like the obvious problem, but there is a more insidious driver in this financial train wreck.

Finance professor Shahid Hamid, who directs the Laboratory for Insurance at Florida International University, explained how Florida’s insurance market got this bad – and how the state’s insurer of last resort, Citizens Property Insurance, now carrying more than 1 million policies, can weather the storm.

What’s making it so hard for Florida insurers to survive?

One is the rising hurricane risk. Hurricanes Matthew (2016), Irma (2017) and Michael (2018) were all destructive. But a lot of Florida’s hurricane damage is from water, which is covered by the National Flood Insurance Program, rather than by private property insurance.

Another reason is that reinsurance pricing is going up – that’s insurance for insurance companies to help when claims spike.

But the biggest single reason is the “assignment of benefits” problem, involving contractors after a storm. It’s partly fraud and partly taking advantage of loose regulation and court decisions that have affected insurance companies.

It generally looks like this: Contractors will knock on doors and say they can get the homeowner a new roof. The cost of a new roof is maybe $20,000-$30,000. So, the contractor inspects the roof. Often, there isn’t really that much damage. The contractor promises to take care of everything if the homeowner assigns over their insurance benefit. The contractors can then claim whatever they want from the insurance company without needing the homeowner’s consent.

If the insurance company determines the damage wasn’t actually covered, the contractor sues.

So insurance companies are stuck either fighting the lawsuit or settling. Either way, it’s costly.

Other lawsuits may involve homeowners who don’t have flood insurance. Only about 14% of Florida homeowners pay for flood insurance, which is mostly available through the federal National Flood Insurance Program. Some without flood insurance will file damage claims with their property insurance company, arguing that wind caused the problem.

How widespread of a problem are these lawsuits?

Overall, the numbers are pretty striking.

About 9% of homeowner property claims nationwide are filed in Florida, yet 79% of lawsuits related to property claims are filed there.

The legal cost in 2019 was over $3 billion for insurance companies just fighting these lawsuits, and that’s all going to be passed on to homeowners in higher costs.

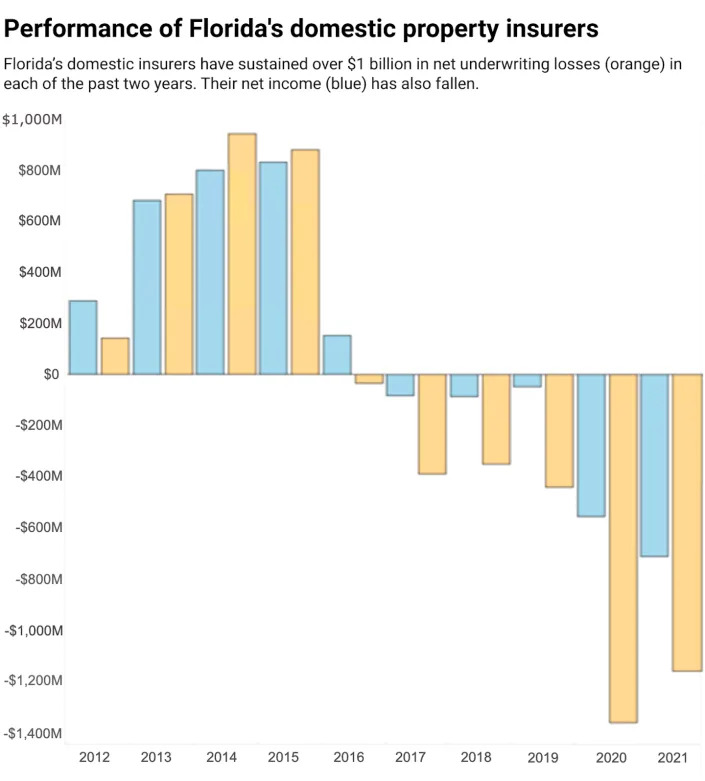

Insurance companies had a more than $1 billion underwriting loss in 2020 and again in 2021. Even with premiums going up so much, they’re still losing money in Florida because of this. And that’s part of the reason so many companies are deciding to leave.

Assignment of benefits is likely more prevalent in Florida than most other states because there is more opportunity from all the roof damage from hurricanes. The state’s regulation is also relatively weak. This may eventually be fixed by the legislature, but that takes time and groups are lobbying against change. It took a long time to pass a law saying the attorney fee has to be capped.

Thirty more are on the Florida Office of Insurance Regulation’s watch list. About 17 of those are likely to be or have been downgraded from A rating, meaning they’re no longer considered to be in good financial health.

Hurricane Ian aftermath: Tour of damage shows parts of Naples look like “a war zone”

Laura Layden, Naples Daily News – October 3, 2022

In a drive around the city, Naples Police Lieutenant Bryan McGinn pointed to some of the worst and costliest damage caused by Hurricane Ian.

On Friday, he whizzed around the city streets, as much as he could, driving through sludge, stopping at every dark traffic light and dodging clean-up and repair crews — and a slew of curious onlookers wanting to see the destruction for themselves.

Scene of Gulf Shore Boulevard North of stranded, flooded cars.

Sludge still filled much of the road, patio furniture lay tangled in the median, cars sat angled in front of condos, a sign of the powerful, unexpected surge that put them completely under water. A crooked boat sat in a parking lot, moved from its perch, with another halfway submerged in waters nearby.

A boat displaced from its dock on Gulf Shore Boulevard North.

Residents had started the clean-up, dragging everything from drenched carpet to soaked couches to the curb. Along with a snarl of landscaping.

Clearly, there’s much more work to be done in the Moorings, Park Shore and elsewhere in the city. With gobs of debris started to make it to the curb.

City residents are picking up the pieces from Hurricane Ian after extreme flooding.

Boats uplifted from their docks

At the Village Shops on Venetian Bay, business owners worked to deal with the mess, a stranded boat sat in the parking lot, with no name on it.

“Unfortunately, there was a lot of water surging,” McGinn said. “That storm came in real fast.”

It wasn’t just water that roared onto the shore in the city. It was loads of sand and sediment from the Gulf of Mexico and Naples Bay, which did plenty of damage of its own.

That sand and sediment turned into a slippery, sticky muck that covered city streets — and the insides of homes and businesses. Some have complained about its stench.

During the tour, McGinn pointed to an extra-wide, steel mobile mini storage container sitting near the intersection of 8th Street South and Broad Avenue, feet from the Cove Inn On Naples Bay, that mysteriously appeared there, likely from a construction site nearby, taking up the entire corner.

“That storage container doesn’t belong there,” he said.

Storage container deposited roadside by surging waters in Naples at 8th Street South and Broad Avenue South.

Its weight is in the thousands of pounds, showing the power of the surge.

In Crayton Cove, McGinn took a turn toward the City Dock, rebuilt a few years ago at a cost of $7 million. He happily reported it fared well.

Businesses are picking up the pieces

Nearby businesses, however, weren’t as lucky, including The Dock, a Naples landmark. It’s still standing, but crews worked busily to clean up its insides, which clearly saw a heavy impact from the storm surge.

Across the way, Napoli On The Bay, didn’t look so good either, with a water line stain halfway up the door.

On Third Avenue South downtown, store owners scrambled to pick up the pieces. Chain saws roared, vacuum trucks rumbled as they sucked out water, and power washers echoed, as owners, employees and hired contractors worked to wash down all the sediment left behind on everything from parking lots to plant pots.

Water stains again showed just how high the water got.

Some business owners have lost virtually everything.

On Third Street and nearby Fifth Avenue South, shops, restaurants and other businesses have scrambled to reopen, if possible.

“Fortunately, our city is resilient,” McGinn said. “So, many business owners are making a push. They want to be able to help people. That’s what they do.”

Businesses are picking up the pieces on Third Street South in downtown Naples.

As soon as it could, Liki Tiki, the local “Tiki Bar” and classic BBQ restaurant on U.S. 41, reopened on Thursday, serving drinks only — because that’s all it could do.

“It was packed,” McGinn said. “It’s a good sight to see. It’s good camaraderie.”

Port Royal may have fared better than others

In Port Royal, known as one of the priciest neighborhoods in America, the damage didn’t seem as great. Signs of water intrusion were harder to spot, but landscaping took a hit, with a near-constant buzz of chain saws.

“A lot of these are new construction homes,” McGinn said. “So, maybe they did fare a little better.”

The Port Royal Club sustained damage.

Closer to the coast, surging waters forced some residents to their roofs, for higher ground, to wait out rescue crews.

“I’m sure there were lives lost,” McGinn said. “But we won’t know how many for some time. It’s hard to tell.”

Some of the stranded cars still spotted around the city, he said, are the result of residents driving around during the storm, failing to heed warnings. They had to walk or swim away, abandoning their vehicles, McGinn said.

“People were still out and about, not listening to shelter in place,” he said, or evacuation orders.

After the storm, vehicles blocking streets were taken to Baker Park, but eventually, the city ran out parking spaces for them.

Mansions on the Gulf could have seen extensive damage

On Gordon Drive, it’s hard to tell how much damage multimillion-dollar mansions sitting directly on the Gulf of Mexico took, but McGinn said the water and sand likely did a lot of damage to them.

Parts of Gordon Drive were still blocked on Friday, with piles of sand dropped by Ian still in the road.

Much of the city saw flooding.

“Even areas like Lake Park had several feet of water in their homes,” McGinn said, after the Gordon River flooded.

The Naples Pier is heavily damaged, but not destroyed.

“It’s sad,” McGinn said.

Treasure hunters and curious visitors at beach, near Naples Pier, damaged by Hurricane Ian, on Friday, Sept. 30, 2022.

While beach ends, or public access points, haven’t reopened, residents and visitors alike have flocked to them, to see the damages with their own eyes shooting photos and videos to document the storm.

“This is how well people listen,” McGinn said. “I get it. Everybody wants to see how the city of Naples fared. It all comes from a good place.”

At the Horizon Way beach access in Park Shore, he pointed to what looked like structural damage at St. Croix Club condominiums, but it was hard to determine the extent of it.

“That’s no bueno,” McGinn said.

Parts of Naples look like a “war zone”

In the Moorings area, Regency Towers looked like it took a heavy hit too — along with other condos and homes.

“It looks like a war zone up here,” McGinn said.

While water wiped out the contents of condos, homes and businesses, he said, structural damage might not be extensive since winds weren’t as extreme as with past storms.

“Their personal property is gone,” McGinn said. “But they can be replaced over time.”

Looking over all the damage in Naples, it’s hard to fathom how bad others had it just one county over, McGinn said.

“What’s crazy is we are not even the hardest hit area,” he said.

‘I just can’t wait to get out’: Nearly three-quarters of pandemic homebuyers have regrets — here’s what you need to know before you put in that offer

Serah Louis – September 30, 2022

‘I just can’t wait to get out’: Nearly three-quarters of pandemic homebuyers have regrets — here’s what you need to know before you put in that offer

Kay Kingsman bought her very first home in the summer of 2021 — but now wishes she hadn’t.

Kingsman, a travel blogger based in Portland, Oregon, says she decided to buy since she had plenty of money saved up from not traveling during the pandemic and mortgage rates were extremely low.

She and many other pandemic homebuyers rushed into making a purchase that didn’t fully align with their needs — and they’re currently contending with the ramifications.

Kingsman recounts finding beard shavings in the bathroom and the carpet smelling of cat urine when the previous owners vacated. The water pressure was weak and the air conditioning was busted.

She also discovered she had no parking privileges thanks to a messy lawsuit they left behind.

“It’s just been a complete headache,” she says.

Many homebuyers either overpaid or made compromises on what they wanted

Nearly three-fourths of Americans who purchased homes in 2021 and 2022 have regrets, according to Anytime Estimate’s American Home Buyer Survey, which was released in September.

“Pandemic-era buyers really faced these unprecedented conditions,” says Amanda Pendleton, home trends expert at Zillow.

“This combination of rising prices, few options to choose from and that extreme time pressure meant that some buyers really ended up at a home that was less than ideal.”

The survey showed that respondents paid a median amount of $495,000 for their home — with almost a third paying over asking.

Eighty percent of buyers also compromised on their priorities, such as finding the right location. Some bought fixer-uppers, while others made offers without even seeing the properties in person.

Like Kingsman, 70% of buyers were purchasing a home for the first time. After seeing a previous listing snapped up within a day, she was determined to not fall behind.

“[Homes] were selling so much above market rate. I didn’t want to wait too long,” explains Kingsman. “And I was kind of swept up in this fast go, go, go motion.”

How can you avoid regretting a home purchase?

Before buying a home, make sure you’ve done your research and established your priorities.

She says that her only priority had been to find a home that was close to her place of work, but wishes she had considered other factors, like updated plumbing and proximity to green spaces and trails.

“I would say my regret is not that I bought a house — it’s more that I didn’t allow myself the time to pick the right house,” says Kingsman.

Pendleton has four tips for house-hunters before buying a home.

“Number one: Before you enter your home search, really understand where you’re willing to compromise and where you’re not,” she says. It’s important to establish your priorities and deal-breakers and separate your needs from your wants ahead of time.

Her second suggestion is to focus on the right things, such as location and layout. “You can update a dated kitchen, you can rip out that ugly carpeting. But all the money in the world really can’t change your home’s location, and changing a home’s layout would be really expensive.”

Pendleton’s third tip is to determine any hidden costs of maintaining the home to make sure you can really afford the home.

She advises not to take any unnecessary risks, such as waiving an inspection. This can end up being incredibly costly later on.

Zillow research shows that homeowners end up paying around $750 a month, or over $9,000 a year just for basic repairs and maintenance.

“The fourth tip would be to have a sounding board,” advises Pendleton. “You know, you really want to rely on a trusted real estate agent who will keep you grounded and focused on your priorities … So they can help you identify potential red flags in the home.”

What can you do if you have regrets?

Kingsman doesn’t believe she will ever be completely happy with her current home, mainly because she doesn’t have a designated parking spot and has to resort to parking on the street.

The previous homeowners were embroiled in a conflict with the HOA and one of the stipulations of the resulting lawsuit was that the future owner of the lot wouldn’t have access to designated parking either.

“So now, all my neighbors feel very icky about me because of some drama that they had with the previous owner and my lot,” adds Kingsman.

She hopes to eventually sell or rent out the home.

“I feel like a lot of people are very sentimental about their first home and stuff, and I just can’t wait to get out.”

Just because you buy a home, doesn’t necessarily mean you’ll never move again.

“Not every home is going to be a forever home,” Pendleton emphasizes. “If your home doesn’t meet your needs, you can always move. And in today’s market, you’re still gonna get a really strong price for your home.”

“Your house may not look like it’s right out of HGTV tomorrow. But you know, if you work on it, maybe in two years, you’re gonna get a lot closer,” she says.

Look into any potential tax credits or rebates you can claim for making upgrades as well, like making energy efficient improvements.

Today’s homebuyers may have better luck

If you can afford today’s mortgage rates and prices, you might be in a better place than buyers were in the past couple years.

The housing market has shown signs of cooling — with home sales dropping for the seventh month in a row and prices falling for the first time in a decade.

“The silver lining for [buyers] is that they are going to be facing less competition, they’re probably not going to get into a heated bidding war, they’re going to have more options to choose from, they’re going to have a little bit more breathing room to make that decision,” says Pendleton.

This article provides information only and should not be construed as advice. It is provided without warranty of any kind.

Hurricane Ian could cripple Florida’s home insurance industry

Alexis Christoforous – September 29, 2022

Hurricane Ian could cripple Florida’s already-fragile homeowners insurance market. Experts say a major storm like Ian could push some of those insurance companies into insolvency, making it harder for people to collect on claims.

Since January 2020, at least a dozen insurance companies in the state have gone out of business, including six this year alone. Nearly 30 others are on the Florida Office of Insurance Regulation’s “Watch List” because of financial instability.

“Hurricane Ian will test the financial preparedness of some insurers to cover losses to their portfolios, in particular smaller Florida carriers with high exposure concentrations in the impacted areas,” Jeff Waters, an analyst at Moody’s Analytics subsidiary RMS and a meteorologist, told ABC News. Waters said Florida is a peak catastrophe zone for reinsurers, and those with exposure will likely incur meaningful losses.

PHOTO: This aerial photo shows damaged homes and debris in the aftermath of Hurricane Ian, Sept. 29, 2022, in Fort Myers, Fla. (Wilfredo Lee/AP)

More than 1 million homes on the Florida Gulf Coast are in the storm’s path, and while Ian’s track and severity can change in the coming days, one early estimate pegs the potential reconstruction cost at $258 billion, according to Corelogic, a property analytics firm.

Industry analysts say years of rampant and frivolous litigation and scams have brought Florida’s home-insurance market to its knees, with many large insurers like Allstate and State Farm, reducing their exposure to the state in the past decade.

“Insurers most exposed to the storm will be the Florida-only insurers, which we define as insurance companies with at least 75% of their homeowners and commercial property premiums written in Florida,” according to a report from Moody’s Analytics submitted to ABC News.

The state-run, taxpayer-subsidized Citizens Property Insurance Corp. stands to lose the most. As more local insurance companies in Florida have closed their doors, Citizens has seen its number of policyholders swell from 700,000 to more than 1 million in just the past year.

Florida state Sen. Jeff Brandes, a Republican from St. Petersburg and a vocal critic of Florida’s insurance industry, warns that if Citizens can’t pay its claims, Floridians should brace for assessments to go up on their own insurance policies under a state law that allows it to assess non-customers to pay out claims.

“Every policy holder in the state of Florida, home and auto, should be watching this storm very carefully because it could have a direct impact on their pocketbooks,” said Brandes. He predicts policy holders will see rate hikes of up to 40% next year as a result of Ian.

A spokesperson for Citizens tells ABC News that if their preliminary estimate of 225,000 claims and $3.8 billion in losses holds, the insurer of last resort would be in a position to pay all claims without having to levy a “hurricane tax” on residents.

Florida is already home to the highest insurance premiums in the U.S., something Charlie Crist, the former Florida governor running against incumbent Gov. Ron DeSantis, blames on his opponent.

“Gov. DeSantis let these insurance companies double Floridians’ rates and they’re still going belly up when homeowners need them most. You pay and pay and pay, and the insurance company isn’t there for you in the end anyway,” Crist said in a statement Monday.

A spokesperson for DeSantis did not immediately respond to ABC News’ request for comment.

In May, DeSantis signed a bipartisan property insurance reform bill into law that poured $2 billion into a reinsurance relief program and $150 million into a grant program for hurricane retrofitting. Among other things, it prohibits insurance companies from denying coverage based on the age of a roof and limits attorney fees on frivolous claims and lawsuits.

At a news conference Tuesday, DeSantis said a lot of the damage from Ian would be from flooding and storm surge. DeSantis said the danger with the Tampa Bay area is that the water has no place to go, noting that the area has close to 1 million residents enrolled in a national flood insurance program.

PHOTO: A man begins cleaning up after Hurricane Ian moved through the Gulf Coast of Florida on Sept. 29, 2022 in Punta Gorda, Fla. (Win Mcnamee/Getty Images)

Homeowner policies typically do not cover flood damage, and most homeowners located in a flood zone often get coverage from the Federal Emergency Management Agency (FEMA). Most private property insurance companies insure primarily for wind damage.

President Joe Biden on Thursday approved DeSantis’ request for a disaster declaration for a number of counties in the state. It includes grants for temporary housing and home repairs and low-cost loans to cover uninsured property losses.

“The expense will be higher because of higher construction costs and overall inflation,” Denise Rappmund, the vice president of Moody’s Public Project and Infrastructure Finance Group, told ABC News. “FEMA is the key source of aid following a natural disaster, but much of the costs to repair and rebuild damaged property will be borne by property insurers who will benefit from $2 billion of state-funded reinsurance.”

Analysts say Hurricane Ian has the potential to be among the four costliest storms in U.S. history, mostly because Florida’s population has exploded in recent years.

No state in the eastern U.S. has grown faster in population than Florida in the past decade and the state’s fastest growing cities: Tampa, Fort Myers and Sarasota, are all in the storm’s path. Analysts warn that more people and more homes mean that a major storm could become more destructive and costly.