Read About The Tarbaby Story under the Category: About the Tarbaby Blog

Author: John Hanno

Born and raised in Chicago, Illinois. Bogan High School. Worked in Alaska after the earthquake. Joined U.S. Army at 17. Sergeant, B Battery, 3rd Battalion, 84th Artillery, 7th Army. Member of 12 different unions, including 4 different locals of the I.B.E.W. Worked for fortune 50, 100 and 200 companies as an industrial electrician, electrical/electronic technician.

What Floridians are enduring is decades in the making. Agricultural runoff polluting the water and Big Sugar blocking its natural flow. Bianca Graulau with 10News in Tampa Bay does a remarkable job telling the story here.

Like George was calling out Big Sugar by name: “They spend billions of dollars every year lobbying, lobbying, to get what they want. Well, we know what they want. They want more for themselves and less for everybody else.

But I’ll tell you what they don’t want: They don’t want a population of citizens capable of critical thinking. They don’t want well informed, well educated people capable of critical thinking. They’re not interested in that. That doesn’t help them. That’s against their interests.”

Like George was calling out Big Sugar by name: “They spend billions of dollars every year lobbying, lobbying, to get what they want. Well, we know what they want. They want more for themselves and less for everybody else. But I'll tell you what they don’t want: They don’t want a population of citizens capable of critical thinking. They don’t want well informed, well educated people capable of critical thinking. They’re not interested in that. That doesn’t help them. That’s against their interests.”

Despite Trump and Scott Pruitt, the world is making progress to address climate change. Costa Rica is proving that it’s possible to rapidly transition away from fossil fuels to renewable energy. (via The Years Project)

Despite Trump and Scott Pruitt, the world is making progress to address climate change. Costa Rica is proving that it's possible to rapidly transition away from fossil fuels to renewable energy. (via The Years Project)

And for good reason: A shocking 21 percent of Americans have nothing at all saved for the future, and another 10 percent have less than $5,000 tucked away, the study finds.

That means about a third of Americans have only a few thousand dollars, or less, put away for their golden years.

Of course, some people are more prepared: A quarter report having $200,000 or more stashed away, while 16 percent have between $75,000 and $199,999. But overall, Northwestern Mutual found that Americans with retirement savings have an average of $84,821 saved, which is far from enough. Experts typically recommend trying to accumulate at least $1 million.

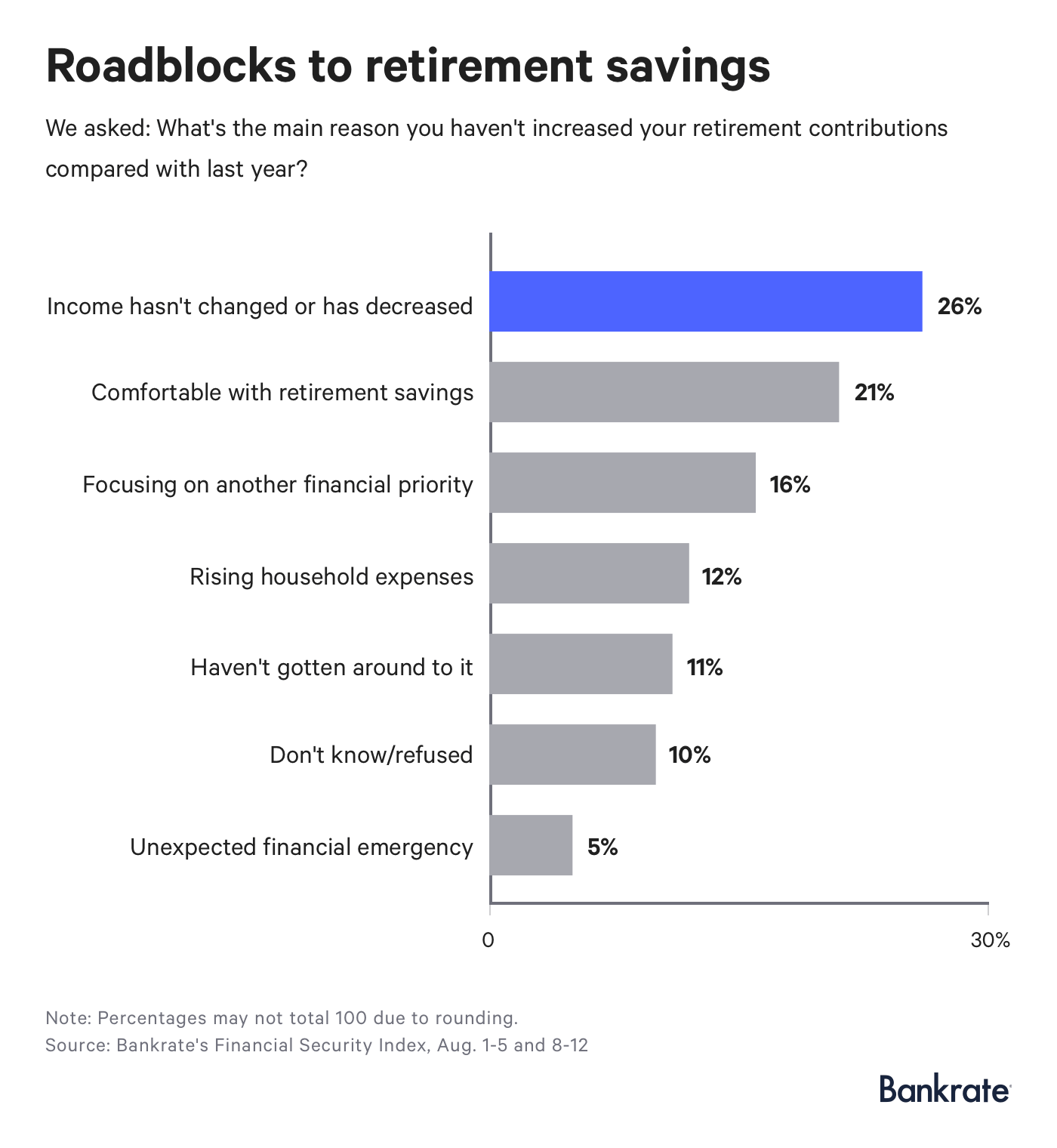

Meanwhile, a new survey from Bankrate finds that 13 percent of Americans are saving less for retirement than they were last year and offers insight into why much of the population is lagging behind. The most popular response survey participants gave for why they didn’t put more away in the past year was a drop, or no change, in income.

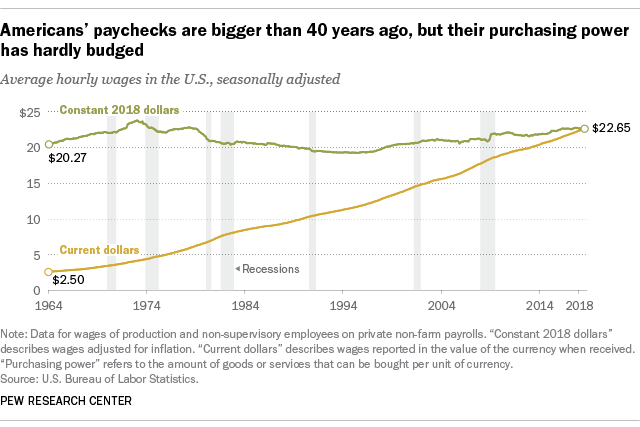

“That’s consistent with federal data that show real wages have barely budged in decades,” Bankrate reports. According to the Pew Research Center, the average paycheck has the same purchasing power it did 40 years ago.

Day-to-day costs continue to soar, and salaries don’t go as far as they once did to cover the necessities, author and executive director of the Economic Hardship Reporting Project Alissa Quart tells CNBC Make It. That makes it more difficult to set aside money for the future.

The good news is there are ways to make progress without feeling cash-strapped or committing to any drastic lifestyle changes. Here are three effective strategies:

1. Start ASAP. The sooner you begin putting your money to work, the less you’ll have to save each month to reach your goals, thanks to the power of compound interest.

If you start at age 23, for instance, you only have to save about $14 a day to be a millionaire by age 67. That’s assuming a 6 percent average annual investment return. If you start at age 35, on the other hand, you’d have to set aside $30 a day to reach seven-figure status by age 67.

Here’s how much you should save at every age.

2. Automate. If you automate your retirement savings — meaning, you have a portion of your paycheck sent directly to a retirement account, such as a 401(k), Roth IRA or traditional IRA — you’ll never even see the money you’re setting aside and will learn to live without it.

Check online to see if you can set up “auto-increase,” which allows you to choose the percentage you want to raise your contributions by and how often. This way, you won’t forget to up your contributions or talk yourself out of setting aside a larger chunk when the time comes.

If you can’t find the feature online, call your retirement plan provider to find out what’s possible.

3. Bank any surplus money. Whenever you come across any extra cash — a bonus, birthday check or small windfall — rather than blowing it on a new pair of shoes or a vacation, send at least a chunk of it straight to savings.

To resist the temptation to spend any surplus money, deposit it right away, so you never even see it.

Student loan watchdog quits: Trump admin ‘turned its back on young people’

Katie Krzaczek August 27, 2018

Women have more student loan debt

The U.S. government official overseeing the protection of student loan recipients from predatory lending practices resigned at the Consumer Financial Protection Bureau (CFPB) and wrote a scathing letter addressed to Mick Mulvaney, the bureau’s acting director.

As first reported by NPR, who obtained the letter, Seth Frotman asserted that Mulvaney’s leadership led the bureau to “[abandon] the very consumers it is tasked by Congress with protecting.”

The CFPB under Mulvaney’s leadership, Frotman wrote, “has turned its back on young people and their financial futures.”

Mick Mulvaney reacts as he attends the daily briefing at the White House in Washington, U.S., July 20, 2017. REUTERS/Carlos Barria

The CFPB oversees financial practices that could potentially harm consumers.

“We protect consumers from unfair, deceptive, or abusive practices and take action against companies that break the law,” the bureau’s website reads.

Part of their protection oversight includes the $1.5 trillion student loan industry. Frotman’s loud resignation brings into question how seriously the government takes its responsibility to protect student borrowers.

Frotman accused Mulvaney of using “the Bureau to serve the wishes of the most powerful financial companies in America.”

The cost of getting a degree contributes a large part to that burden. From the time that millennials were born until the time they entered college, tuition increased by nearly 129% for private colleges and by over 213% for public colleges, when adjusted for inflation.

Add that to the fact that, according to a new St. Louis Fed study, families of millennials were hit particularly hard by the Financial Crisis. (Single millennials aren’t doing much better.)

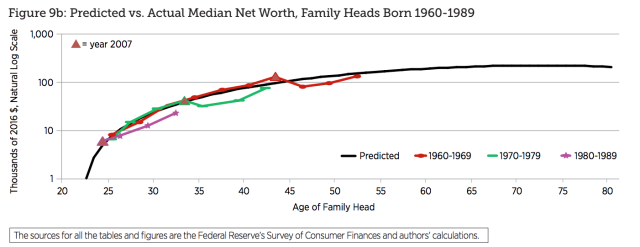

“Wealth in 2016 of the median family headed by someone born in the 1980s remained 34 percent below the level we predicted based on the experience of earlier generations at the same age,” the Federal Reserve Bank of St. Louis stated.

Predicted vs. Actual Median Net Worth, Family Heads Born 1960–1989. Federal Reserve Bank of St. Louis.

“Consider a typical 32-year-old family respondent in 2016 (born in 1984),” the study added. “This respondent’s family was 34 percent ($12,000) below the 32-year-old benchmark established by earlier generations.” This group is also holding more debt than any previous generations.

And because the debt that millennial families hold is not attached to “assets that have appreciated rapidly during the last few years — such as stocks and real estate — they have received no leveraged wealth boost like that enjoyed by older cohorts.” Instead, this group is dealing with debts that accumulate high interest in a seemingly never-ending cycle of repayment, such as credit card debt, auto loans, and, yes, student loans.

Seth Frotman. (Photo: CFPB)

Losing an advocate

Frotman had served at the CFPB since the agency was started seven years ago, and he held the position of ombudsman for the last three years. There, he was in charge of the Office for Students and Young Consumers, where he reviewed complaints from student borrowers about private lenders, loan servicers, and debt collectors.

His departure comes after the relationship between the Trump administration and the CFPB has grown increasingly fraught.

Last summer, the U.S. Department of Education announced it would no longer share information regarding the oversight of federal student loans with the CFPB, claiming the bureau was “overreaching and unaccountable.”

“The Bureau’s current leadership folded to political pressure … and failed borrowers who depend on independent oversight to halt bad practices,” Frotman wrote of the decision.

Here’s how this North Carolina couple could retire in their 30’s.

Here’s how this North Carolina couple could retire in their 30’s.